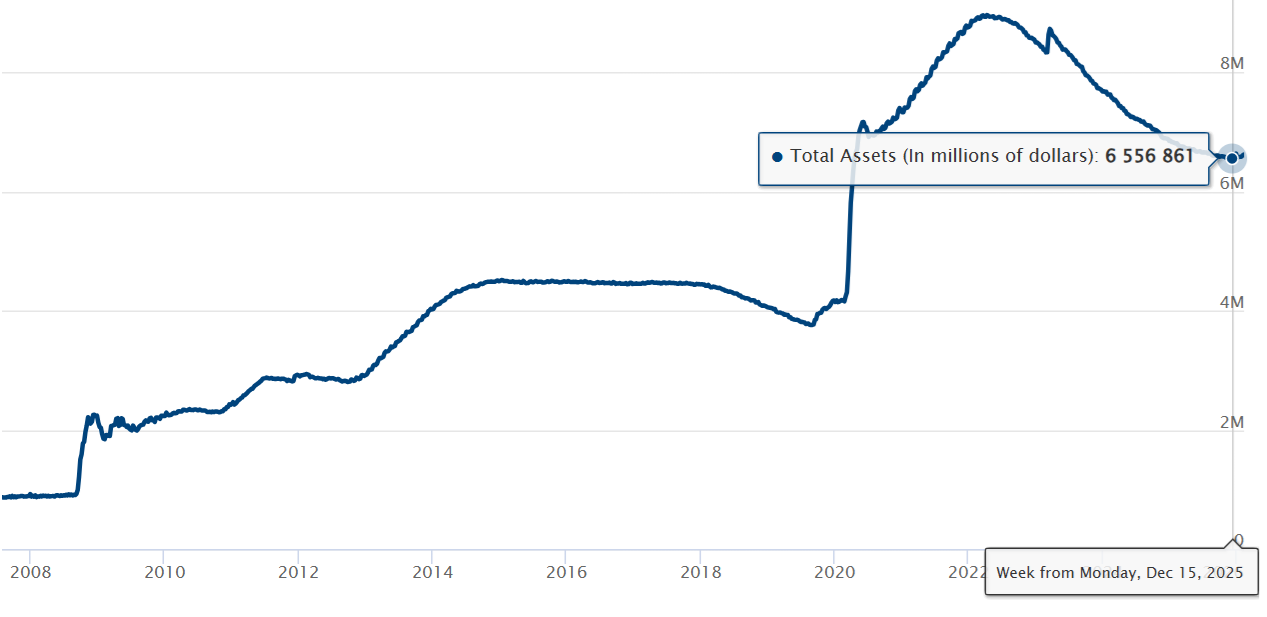

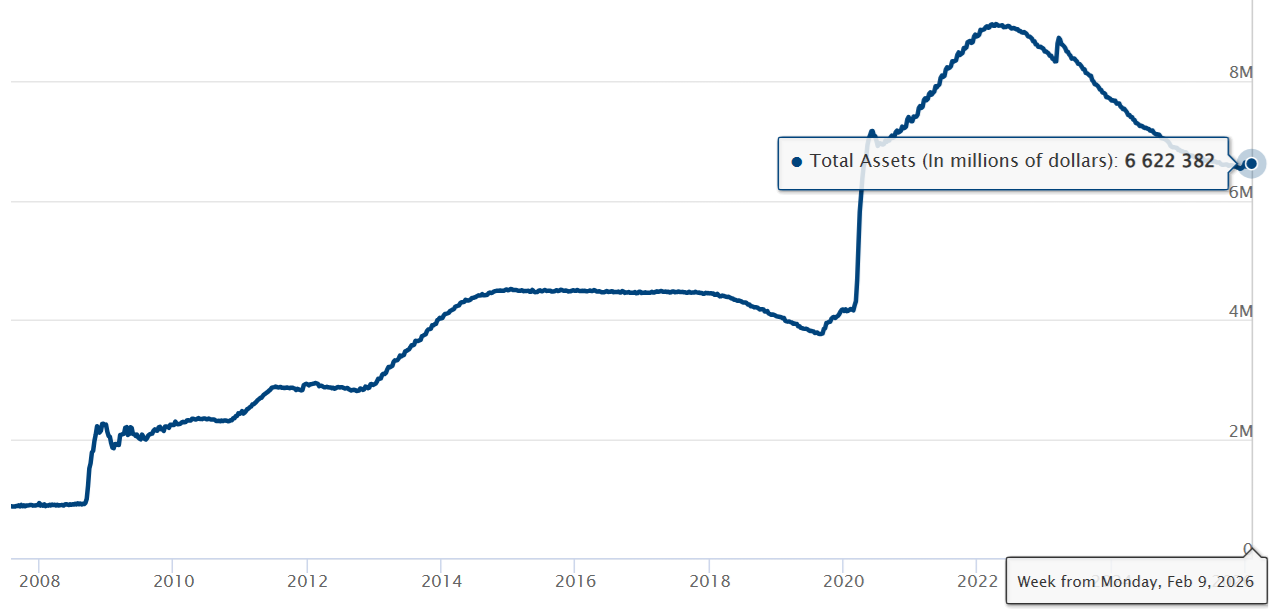

The iShares 0-3 Month Treasury Bond ETF (SGOV) is an ETF that seeks to track an index that includes U.S. Treasury bills with maturities of 0–3 months. Thus it holds investments what effectively become cash in 90 days.

Net Assets of Fund = $99,949,124,843 ($99 Billion).

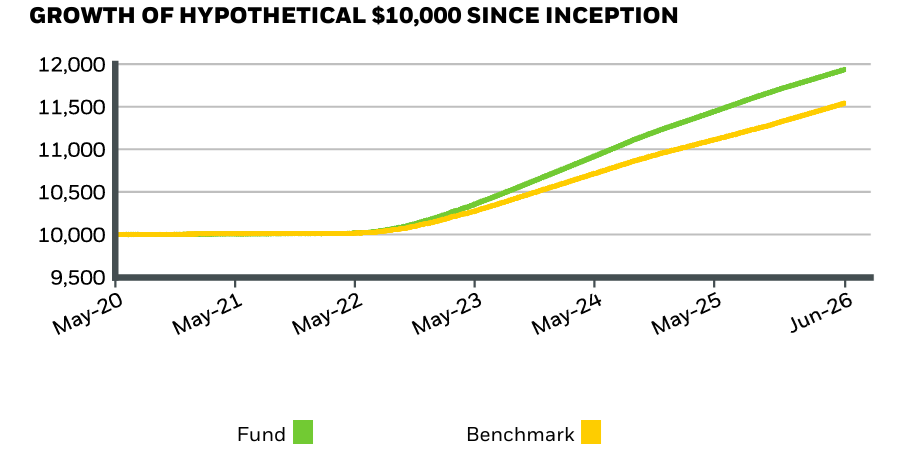

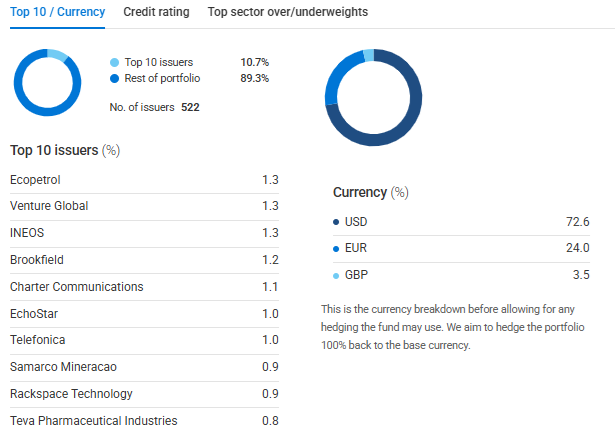

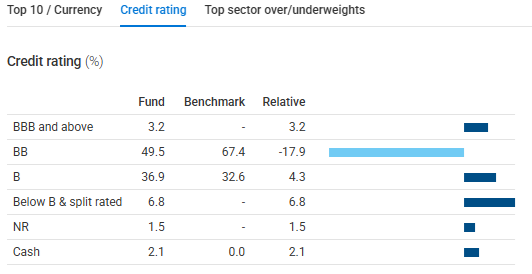

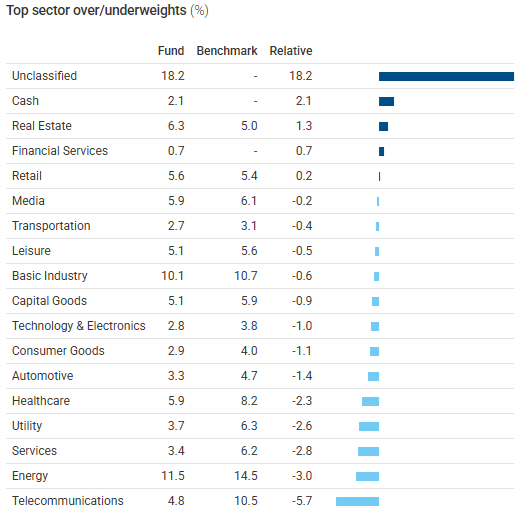

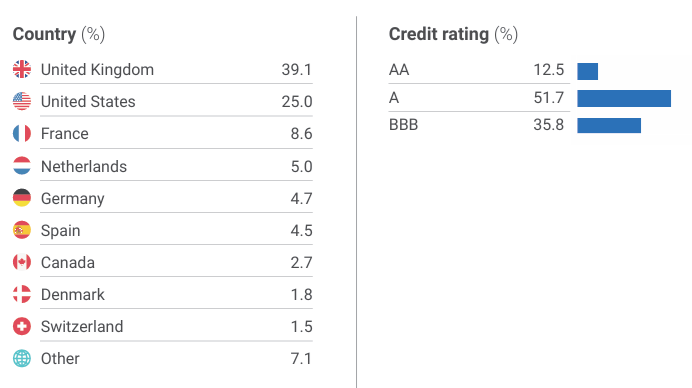

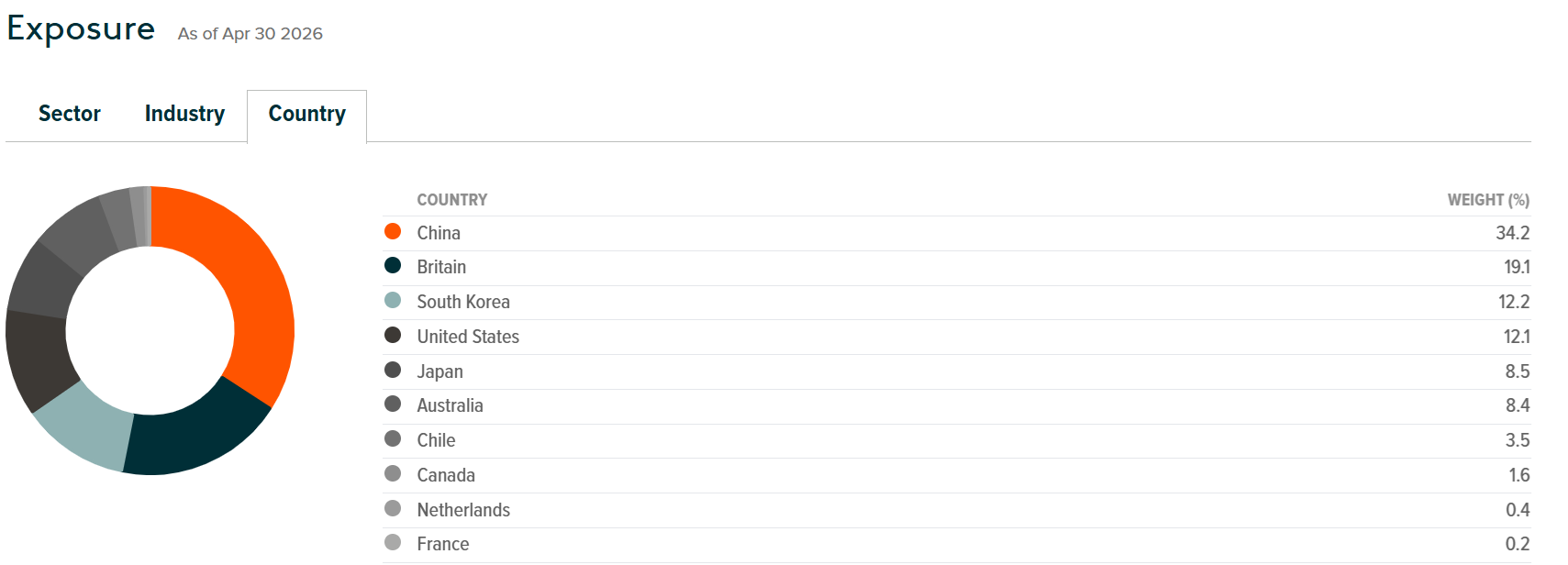

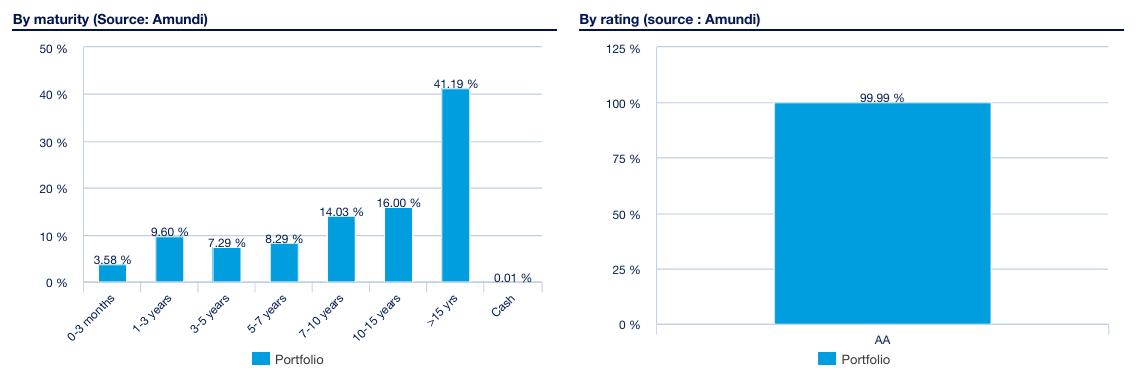

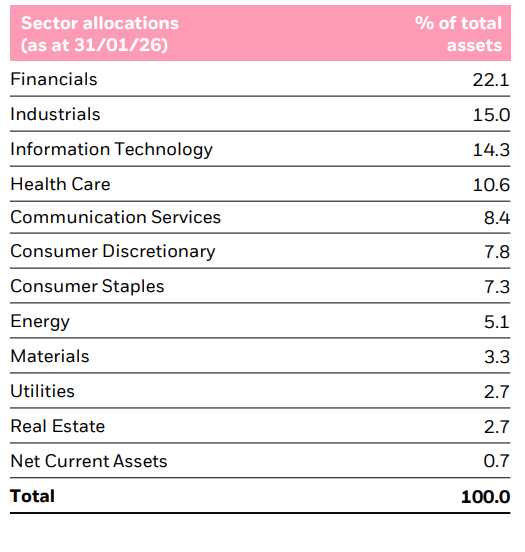

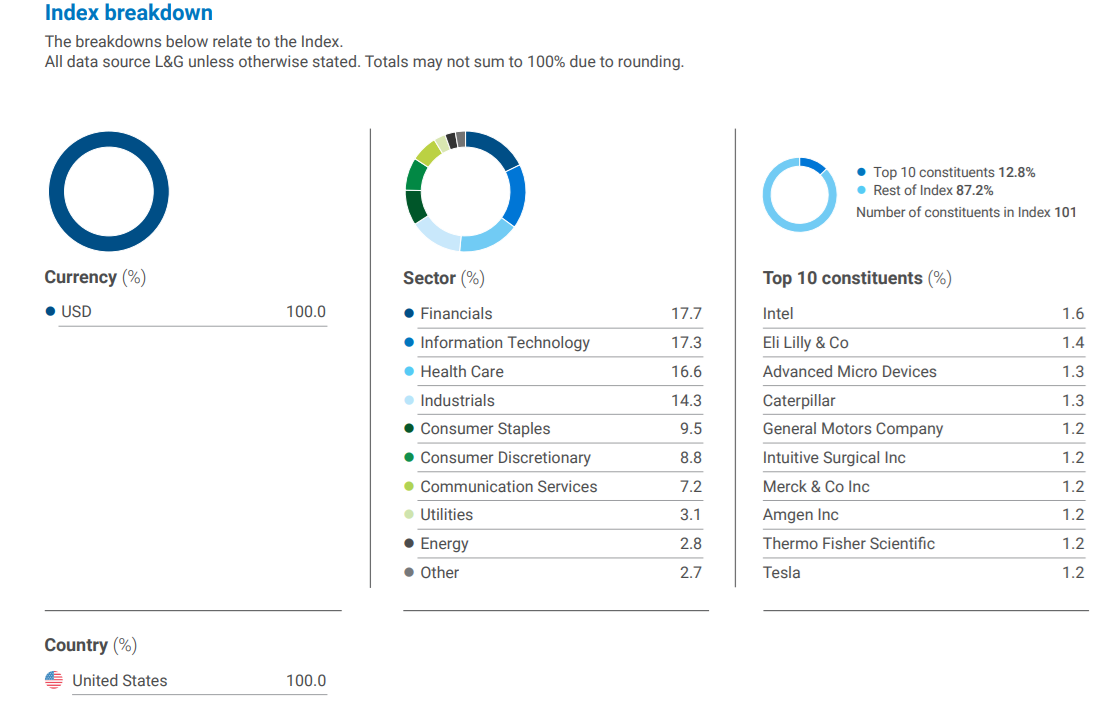

The L&G Global High Yield Bond Fund has the objective to provide a combination of capital growth and income over the long term. The Fund is actively managed and seeks to achieve this objective by investing at least 80% of its assets in a broad range of fixed income securities from around the world. The Fund aims to deliver this objective while maintaining a lower weighted average carbon intensity than the Benchmark Index.

Fund size (20 Jul 2026)

$932.2m

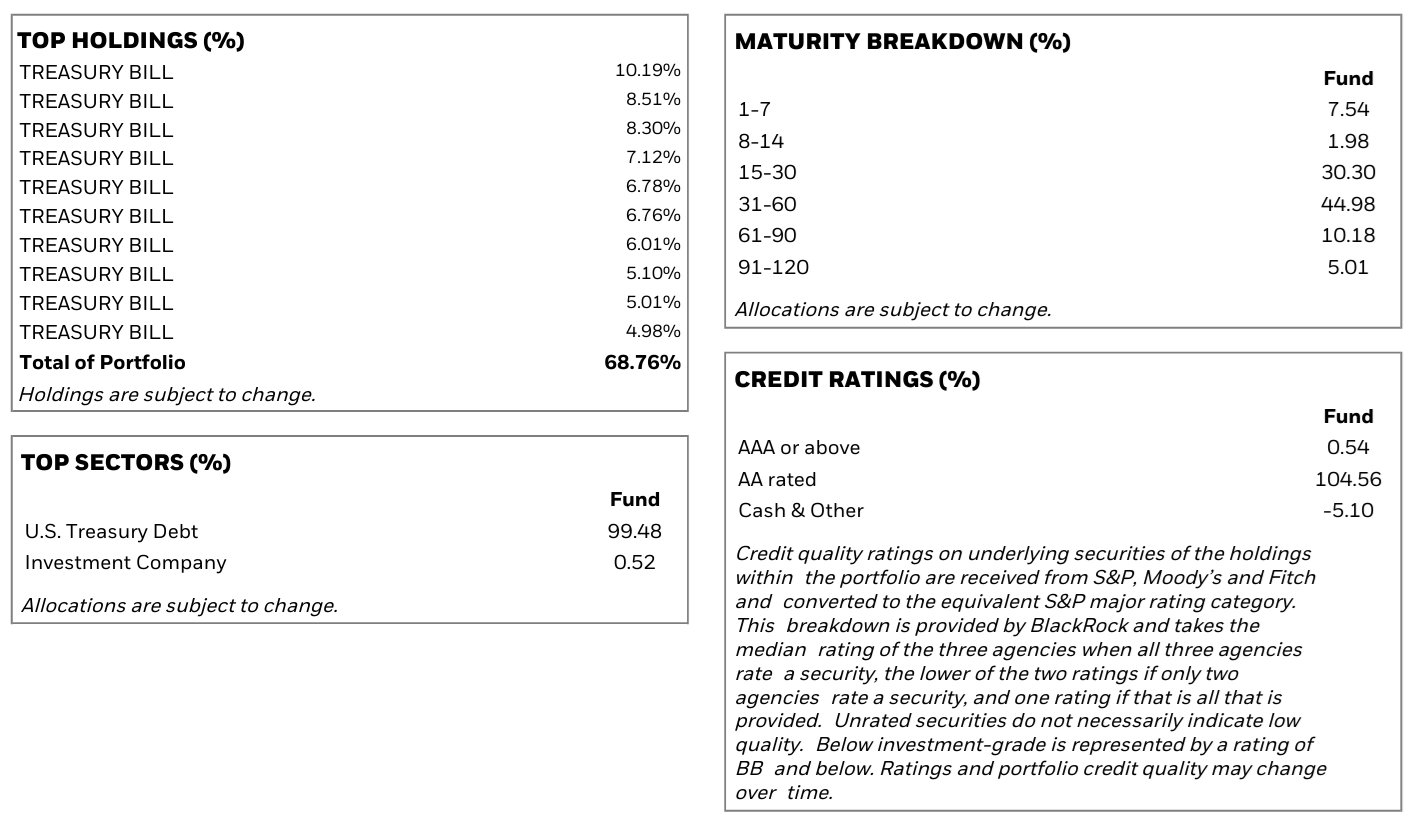

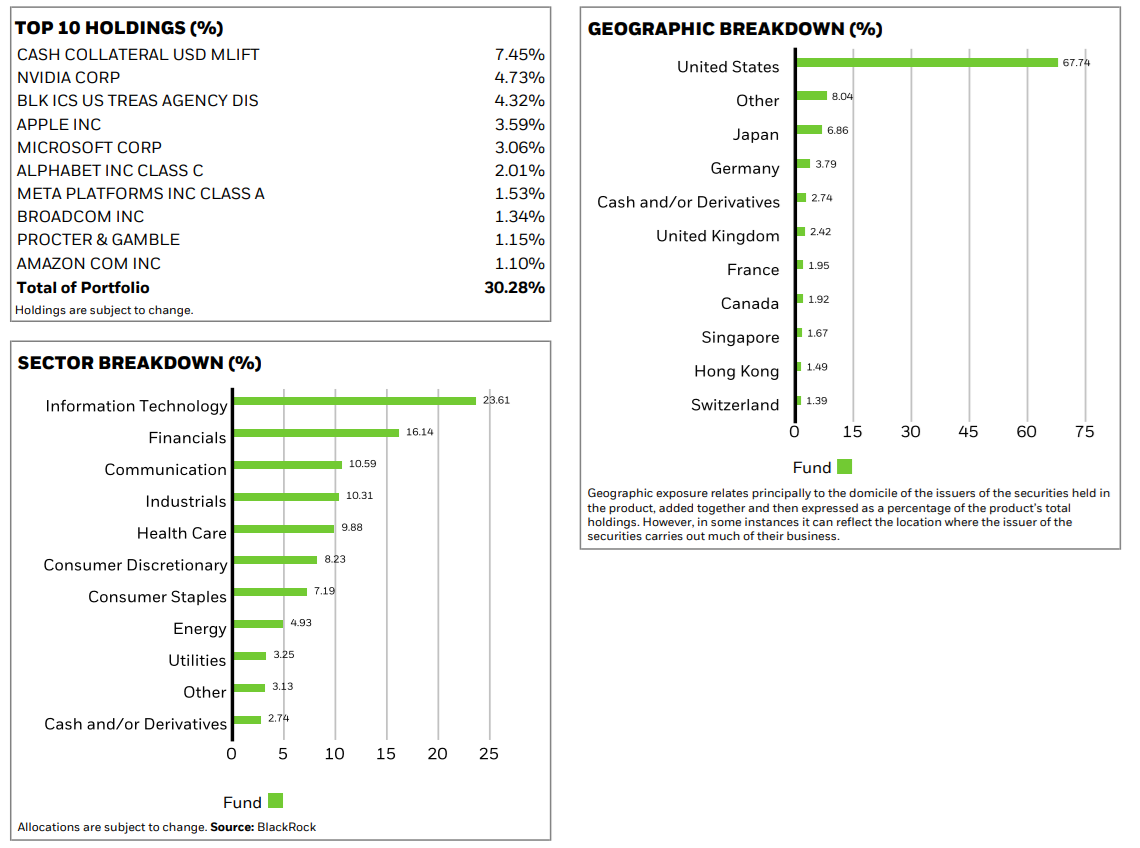

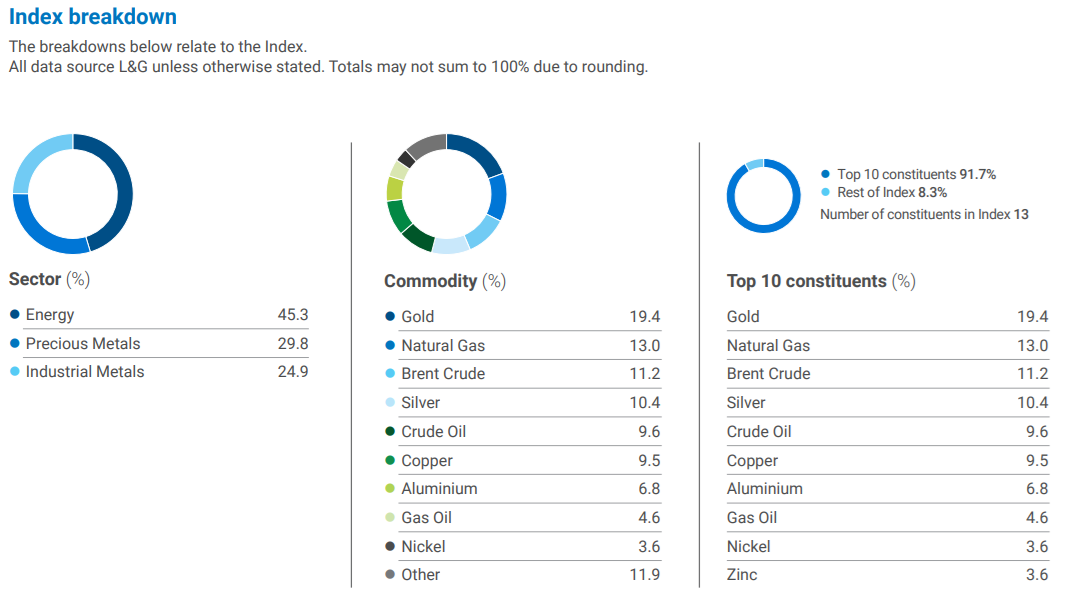

Courtesy of Legal and General Investment Management

Courtesy of Legal and General Investment Management

Courtesy of Legal and General Investment Management

Courtesy of Legal and General Investment Management

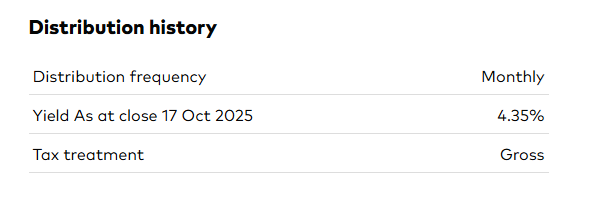

The Legal & General Cash Trust is a fund that is designed for investors looking to preserve their money from an investment in deposits and short term instruments.

This fund may be appropriate for investors looking to invest for a short period of time.

Fund size: £4,236.7m

Courtesy of Legal and General Investment Management

Courtesy of Legal and General Investment Management

Courtesy of Legal and General Investment Management

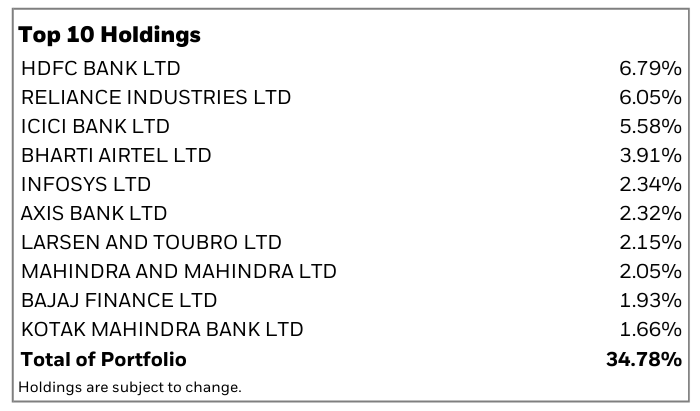

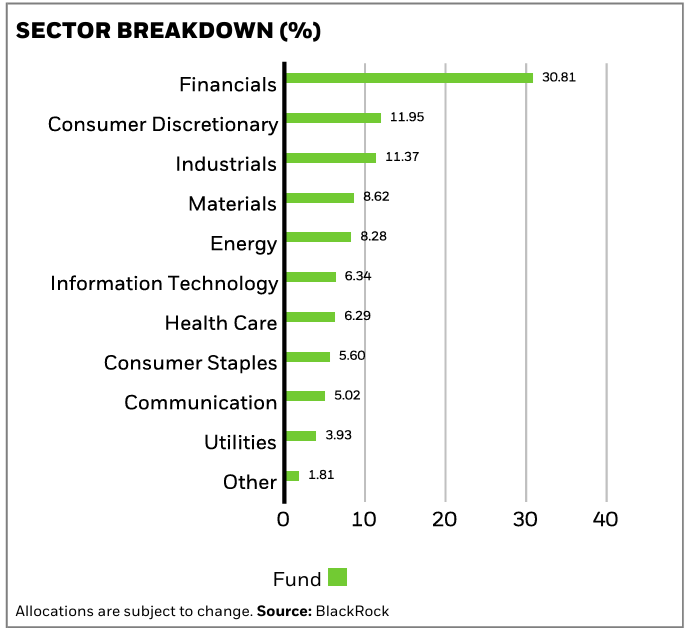

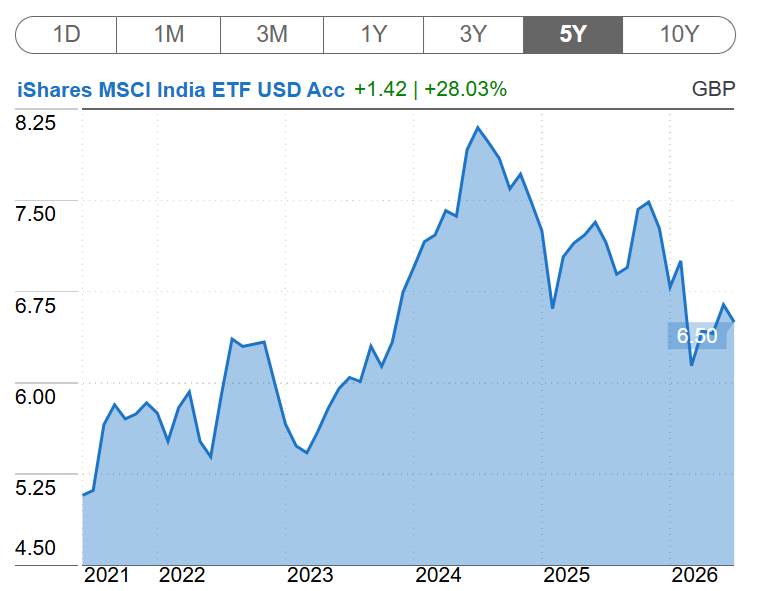

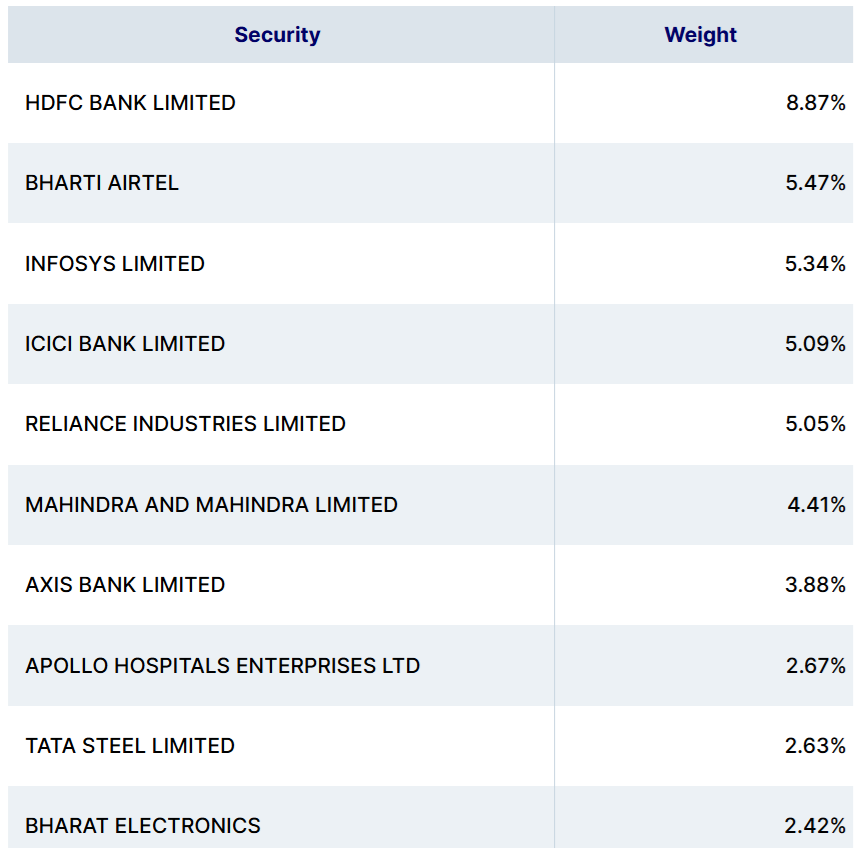

The iShares MSCI India UCITS ETF gives exposure to one of the largest and fastest growing economies in the world, with direct investment into large- and mid-cap stocks covering approximately 85% of the Indian stock market, and can be used as part of a broader equity portfolio to seek growth.

Net Assets of Share Class (Million) : $5130.72 USD

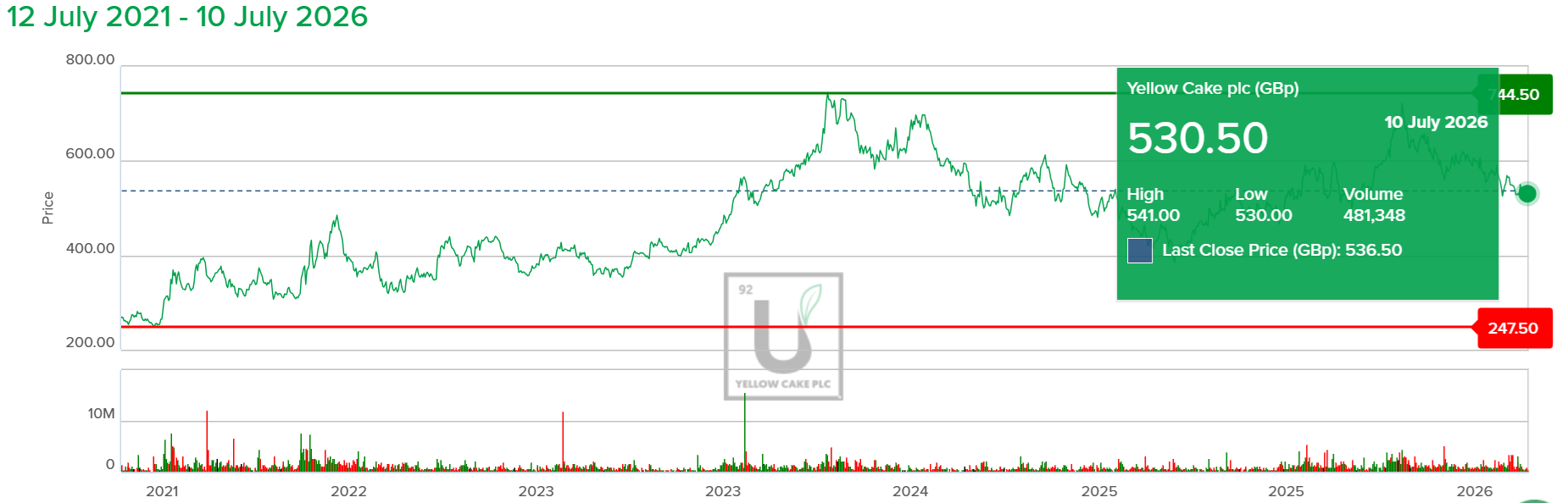

Yellow Cake is a London-quoted company, providing investors with direct exposure to the uranium market through our physical holding of uranium oxide concentrate (U3O8) and by entering into transactions where beneficial commercial opportunities arise from uranium ownership. Yellow Cake’s physical uranium holdings provide an opportunity to profit from an anticipated rise in the uranium price arising from the short- and medium-term supply and demand asymmetry.

WisdomTree Energy Transition Metals is a fully collateralised, UCITS eligible Exchange-Traded Commodity (ETC) designed to provide investors with a total return exposure to a basket of Thematic Metals Baskets futures contracts. The ETC provides a total return comprised of the daily performance of the WisdomTree Energy Transition Metals Commodity Index index (WTETMCTR)

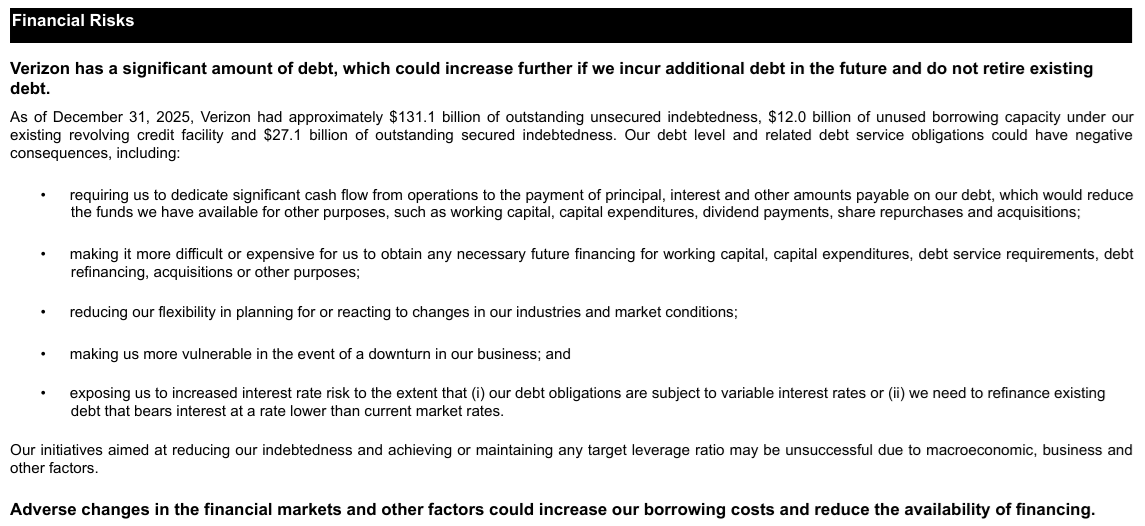

The US Telecommunications giant Verizon, who’s roots can be traced back to the merger of the 2 “baby bells”, NYNEX and Bell Atlantic, today is giant in the global telecommunications landscape.

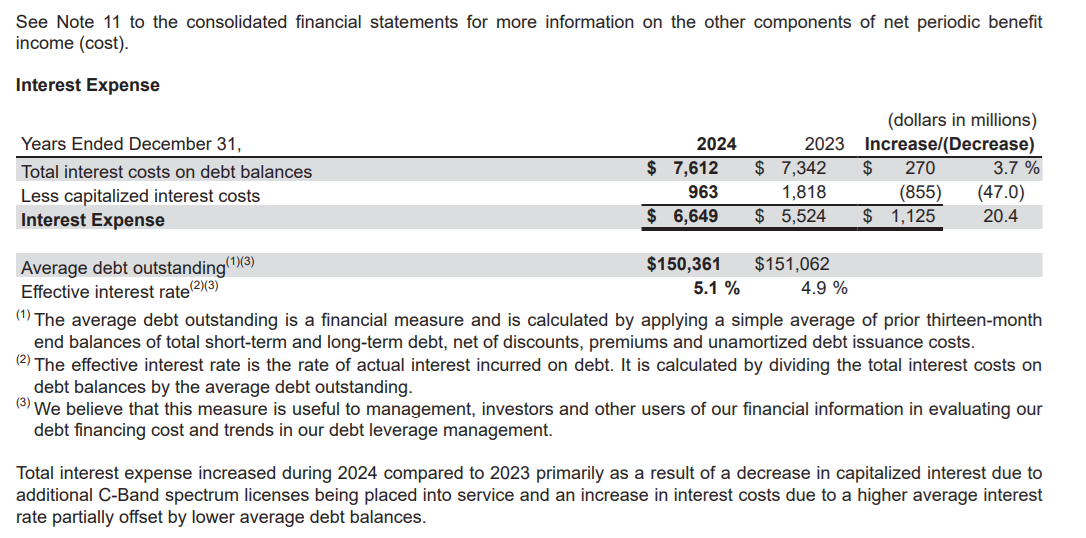

Now the annual report is up to Dec 2025. Debt was stated at $147 Bn, (see below) and then 3 months later, the debt has increased to $177 Bn. In a quarter, the debt has grown by $30 Bn in just 3 months

Courtesy of Verizon.

You can see above, Debt Interest = Financing Costs are $6.694 Billion

From the Income statement we see:-

Courtesy of Verizon

Verizon has revenues of $106 Bn (income) and while the income stream is huge, it still needs $6.694 Bn to simply pay interest on its debt to its Bond Holders (the creditor)

Across developed markets, bond markets are staging a slow-motion car wreck. As Opinion columnist and senior markets editor John Authers puts it, the phenomenon is truly global. Authers and Robin J. Brooks, a senior fellow at the Brookings Institution and former chief economist at the Institute of International Finance, join host Stephanie Flanders to explain why investors have turned sharply against government bonds across the world’s major developed economies — and how the fallout could affect us all.

The Columbia Threadneedle Healthcare Trust PLC, has the investment objective of the Company is to provide shareholders with capital growth and income over the long term, through investment in listed or quoted global healthcare companies.

The Wisdom Tree Megatrends UCITS ETF seeks to track the price and yield performance, before fees and expenses, of the Wisdom Tree Global Megatrends Equity Index.

The L&G GBP Corporate Bond 0-5 Year Screened UCITS ETF (the “ETF”) aims to track the performance of the J.P. Morgan GCI ESG Investment Grade GBP Short-Term Custom Maturity Index. It provides expo sure to the short-term Pound Sterling-denominated investment grade corporate bond market.

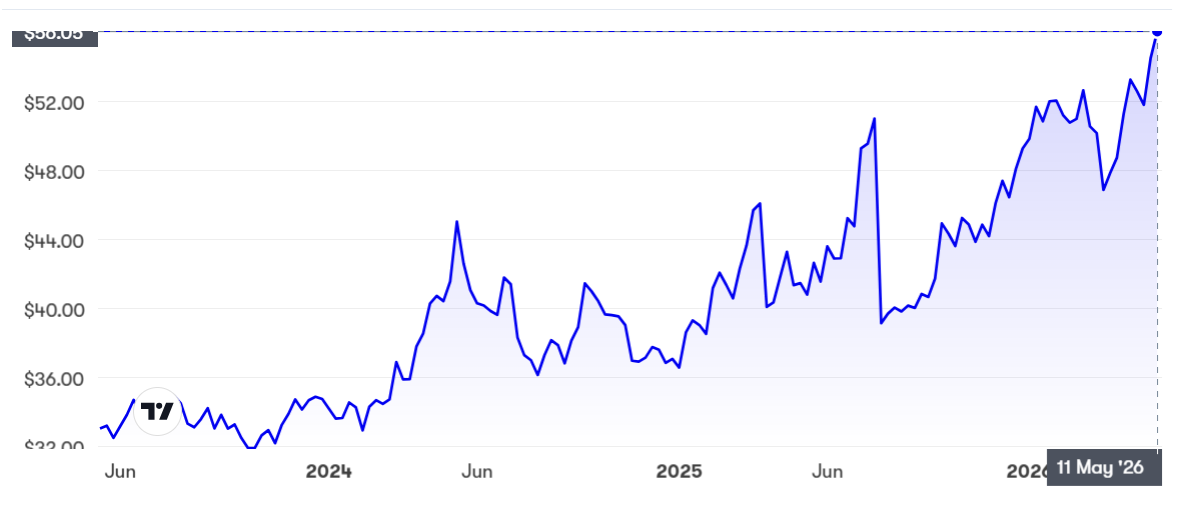

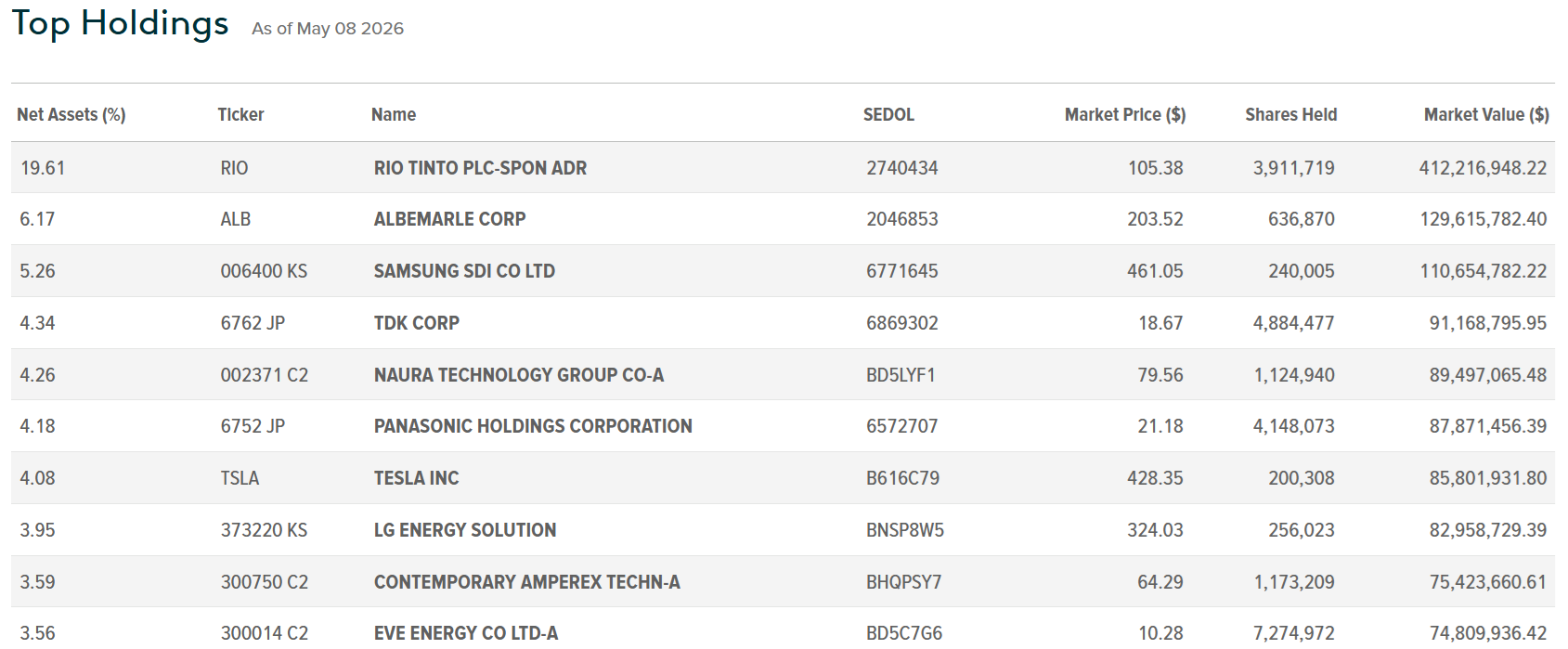

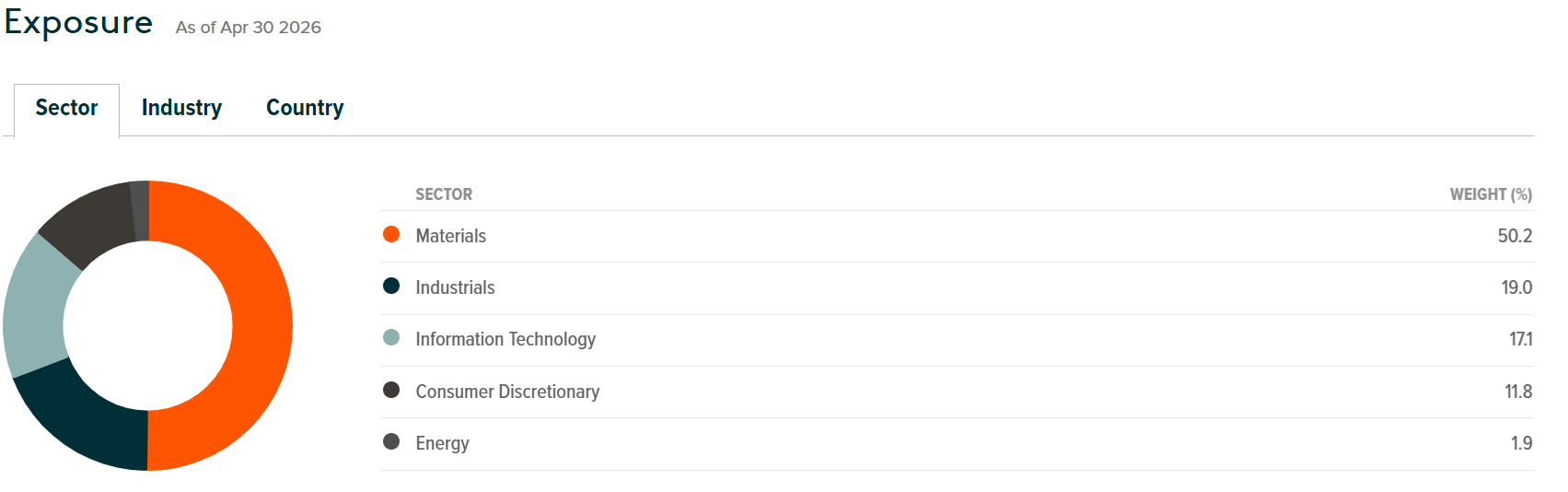

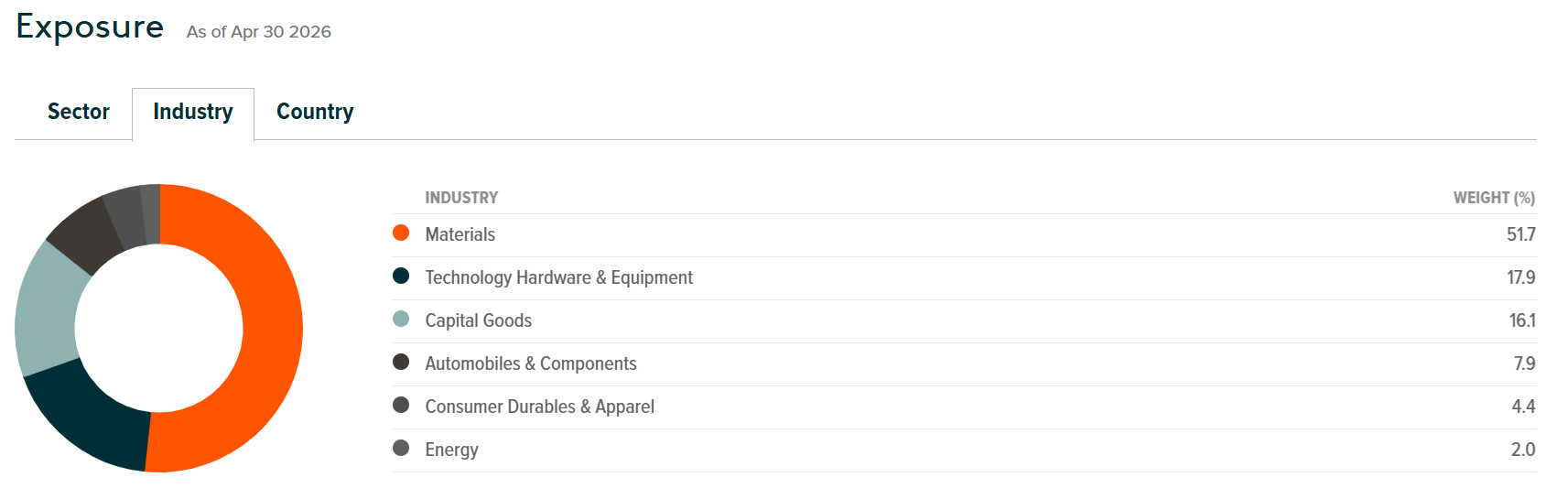

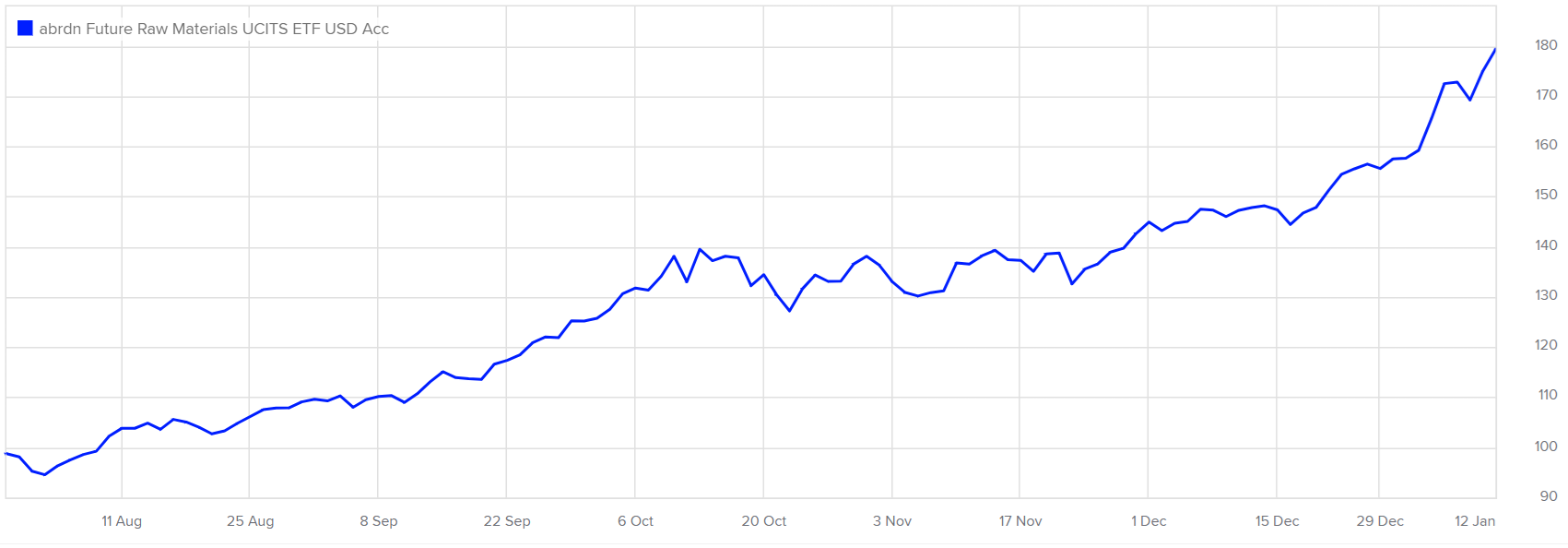

abrdn Future Raw Materials UCITS ETF is a London listed ETF, its investment aim is to generate growth over the long-term (5 years or more) by investing primarily in companies with alignment to the Future Raw Materials Theme.

The Investment Manager actively identifies a short list of key minerals (which may include, but are not limited to, copper, nickel, lithium, aluminium and rare earth minerals)

The WisdomTree Copper ETF is a fully collateralised, UCITS eligible Exchange Traded Commodity (ETC) designed to provide investors with a total return exposure to Copper futures contracts

The Lithium & Battery Tech ETF from Global X invests in the full lithium cycle, from mining and refining the metal, through battery production. The Global X Lithium & Battery Tech ETF (LIT) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Global Lithium Index.

The Kotak Indo-Pacific Defence UCITS ETF (QUAD) aims to provide exposure to Indo-Pacific defence spending, ex-China. China’s military expansion has kick-started the most significant rearmament drive in the Indo-Pacific since the Cold War. In response, countries from India to Japan are not only increasing defence budgets but also accelerating efforts to localise arms production. This shift – from imports to domestic sourcing – presents a growing opportunity for Indo-Pacific defence companies.

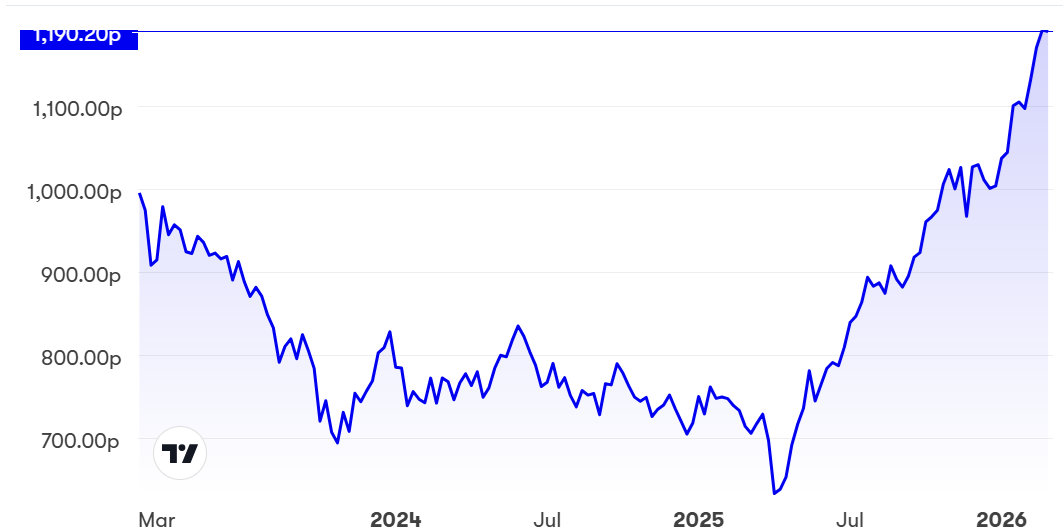

The Legal & General Asia Pacific Equity Income Fund has the objective to provide income in excess of the income generated by the FTSE Asia Pacific ex-Japan TR Net Index, the “Benchmark Index”, measured before the deduction of any charges and over rolling five year periods, whilst aiming for capital growth over the long term (at least five years)

Fund size (31 Mar 2026)

£52.9m

Courtesy of Legal and General Investment Management

Courtesy of Legal and General Investment Management

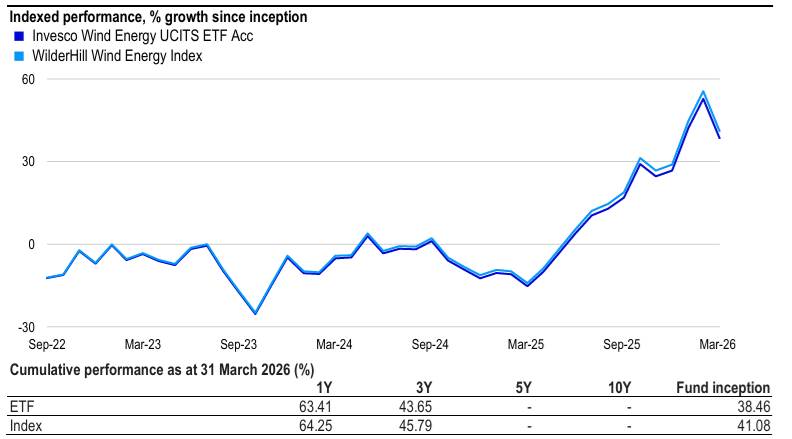

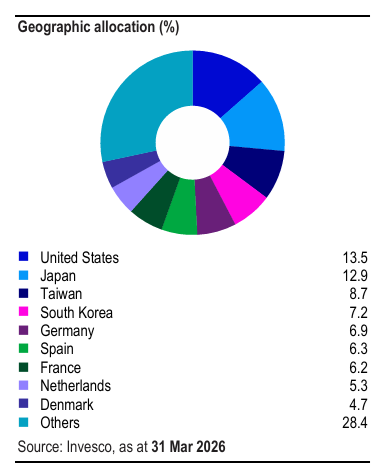

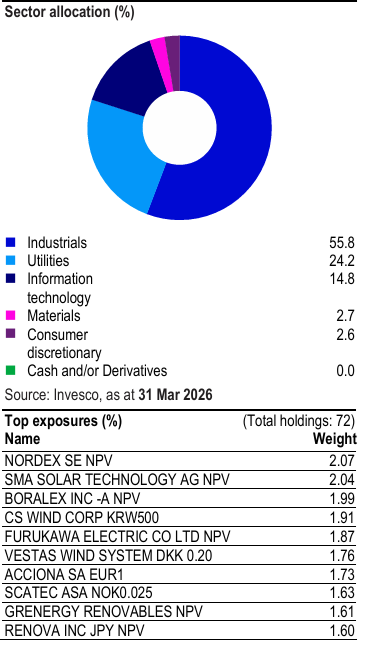

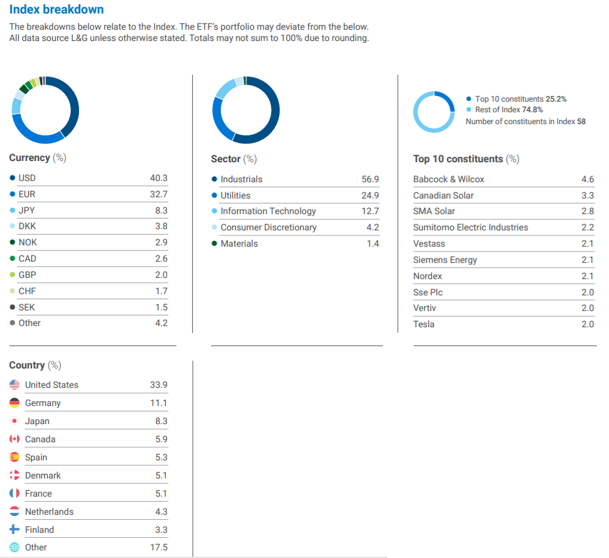

The Invesco Wind Energy UCITS ETF Acc is London listed ETF that aims to track the net total return performance of the WilderHill Wind Energy Net Return Index, less fees.

Courtesy of Invesco.

Courtesy of Invesco

Courtesy of Invesco

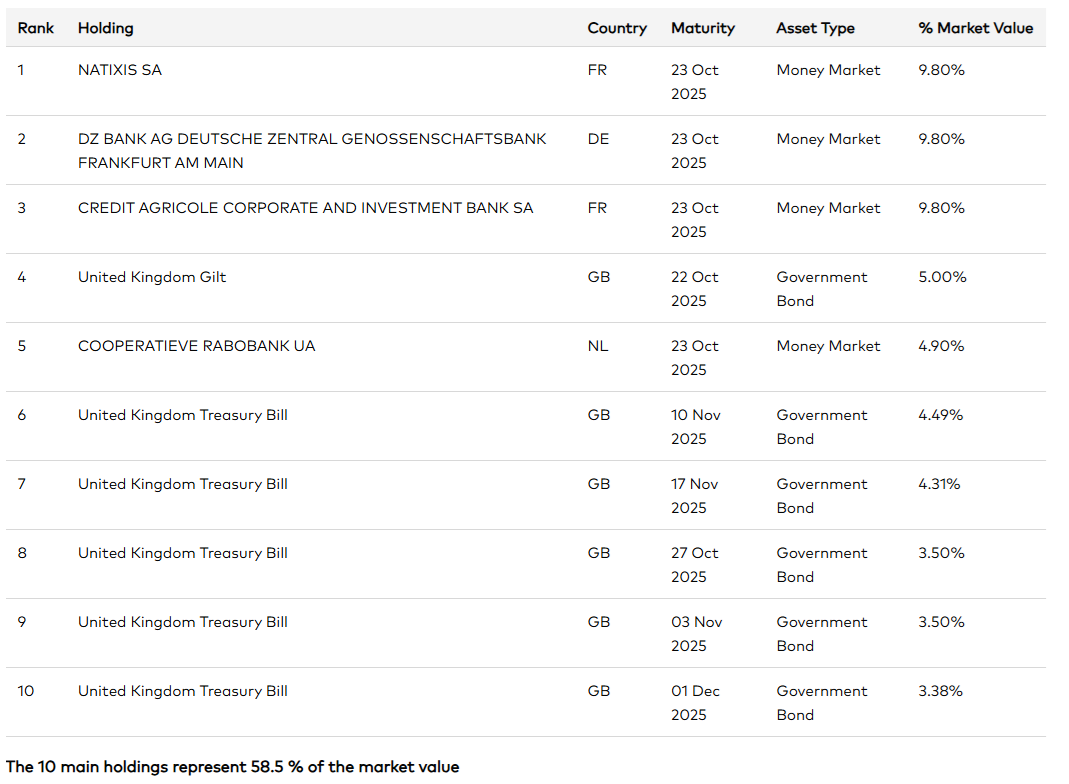

Total Holdings:-

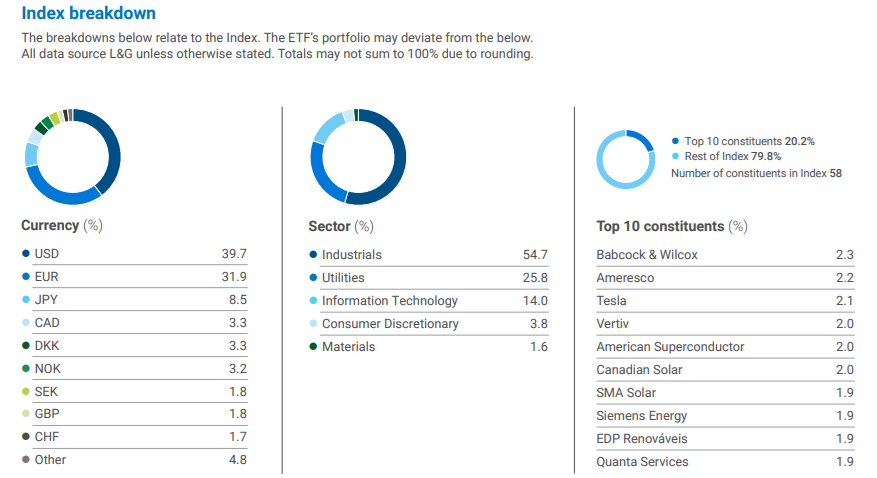

LS ELECTRIC CO LTD KRW5000 KR7010120004 2.6796% Taihan Cable & Solution Co Ltd KRW 1000 KR7001440007 2.3363% FURUKAWA ELECTRIC CO LTD NPV JP3827200001 2.2577% SMA SOLAR TECHNOLOGY AG NPV DE000A0DJ6J9 2.0197% CS WIND CORP KRW500 KR7112610001 1.9346% NORDEX SE NPV DE000A0D6554 1.8689% FUJIKURA LTD NPV JP3811000003 1.8424% RENOVA INC JPY NPV JP3981200003 1.7961% ENLIGHT RENEWABLE ENERGY LTD ILs 0.0100 IL0007200111 1.7151% BORALEX INC -A NPV CA09950M3003 1.7039% OSAKI ELECTRIC CO LTD NPV JP3187600006 1.6793% HD HYUNDAI ELECTRIC & Energy System Co Ltd KRW5000 KR7267260008 1.6453% INFINEON TECHNOLOGIES AG NPV DE0006231004 1.6274% ACCIONA SA EUR1 ES0125220311 1.5958% ALFEN BEHEER B.V. EUR0.1 NL0012817175 1.5607% SINBON ELECTRONICS CO LTD TWD10 TW0003023008 1.5348% PRYSMIAN SPA EUR0.1 IT0004176001 1.5253% VESTAS WIND SYSTEM DKK 0.20 DK0061539921 1.5227% MERSEN EUR2 FR0000039620 1.511% LITTELFUSE INC USD0.01 US5370081045 1.4822% WESCO INTERNATIONAL INC USD0.01 US95082P1057 1.4608% GRENERGY RENOVABLES NPV ES0105079000 1.4429% VAISALA OYJ- A SHS NPV FI0009900682 1.4178% LG ENERGY SOLUTION KRW 500.0000 KR7373220003 1.4134% ORSTED A/S DKK10 DK0060094928 1.4063% ATKORE INC. USD 0.01 US0476491081 1.3963% ENERGIX-RENEWABLE ENERGIES NPV IL0011233553 1.3911% NKT A/S DKK20 DK0010287663 1.385% NEXANS SA EUR1 FR0000044448 1.3821% IMCD NV EUR0.16 NL0010801007 1.3747% SUMITOMO ELECTRIC INDUSTRIES NPV JP3407400005 1.3712% TKH GROUP NV-DUTCH CERT EUR0.25 NL0000852523 1.3632% DAIHEN CORP NPV JP3497800007 1.3588% VALMONT INDUSTRIES USD1 US9202531011 1.3545% CADELER A/S NOK 1.0000 DK0061412772 1.349% TOCALO CO LTD NPV JP3552290003 1.3441% ENERGIEKONTOR AG NPV DE0005313506 1.333% ELIA GROUP NPV BE0003822393 1.3317% WASION GROUP HOLDINGS LTD HKD0.01 KYG9463P1081 1.3131% ARCADIS NV EUR0.02 NL0006237562 1.3094% HYDRO ONE LTD NPV CA4488112083 1.3031% SCATEC ASA NOK0.025 NO0010715139 1.298% EDP RENOVAVEIS SA EUR5 ES0127797019 1.2876% CORP ACCIONA ENERGIAS RENOVA EUR NPV ES0105563003 1.2819% ERG SPA EUR0.1 IT0001157020 1.2809% DEME GROUPEUR NPV BE0974413453 1.2786% SSAB AB-A SHARES SEK8.8 SE0000171100 1.2762% TERNA SPA EUR0.22 IT0003242622 1.2561% HUBBELL INC USD0.01 US4435106079 1.2467% TIMKEN CO NPV US8873891043 1.2435% TOYO TANSO CO LTD NPV JP3616000000 1.2425% LANDIS+GYR GROUP AG CHF10 CH0371153492 1.2396% ALLIS ELECTRIC CO LTD TWD10 TW0001514008 1.2266% SPIE SA EUR0.47 FR0012757854 1.2222% MERIDIAN ENERGY LTD NPV NZMELE0002S7 1.2124% SCHNEIDER ELECTRIC SE EUR4 FR0000121972 1.2038% SHIHLIN ELECTRIC & ENGINEER TWD10 TW0001503001 1.1856% FORTUNE ELECTRIC CO LTD TWD10 TW0001519007 1.1756% REXEL SA EUR5 FR0010451203 1.1691% QUANTUMSCAPE CORP USD 0.0001 US74767V1098 1.1546% TORAY INDUSTRIES INC NPV JP3621000003 1.117% LEM HOLDING SA-REG CHF0.5 CH0022427626 1.1071% VOLTRONIC POWER TECHNOLOGY TWD10 TW0006409006 1.086% JL MAG RARE-EARTH CO LTD -H HKD 1.0000 CNE1000055Y4 1.0855% TECO ELECTRIC & MACHINERY TWD10 TW0001504009 1.0711% TA YA ELECTRIC WIRE & CABLE TWD10 TW0001609006 1.0581% SKF AB-B SHARES SEK2.5 SE0000108227 1.0569% CHINA DATANG CORP RENEWABL-H HKD 1.0000 CNE100000X69 0.9743% BELDEN INC USD0.01 US0774541066 0.9259% FLUENCE ENERGY INC USD 0.0100 US34379V1035 0.8817% WILLDAN GROUP INC USD 0.0100 US96924N1000 0.8062% EOS ENERGY ENTERPRISES INC USD 0.0001 US29415C1018 0.7373% Cash and/or Derivatives -0.0287%

Full name ISIN Weight LS ELECTRIC CO LTD KRW5000 KR7010120004 2.6796% Taihan Cable & Solution Co Ltd KRW 1000 KR7001440007 2.3363% FURUKAWA ELECTRIC CO LTD NPV JP3827200001 2.2577% SMA SOLAR TECHNOLOGY AG NPV DE000A0DJ6J9 2.0197% CS WIND CORP KRW500 KR7112610001 1.9346% NORDEX SE NPV DE000A0D6554 1.8689% FUJIKURA LTD NPV JP3811000003 1.8424% RENOVA INC JPY NPV JP3981200003 1.7961% ENLIGHT RENEWABLE ENERGY LTD ILs 0.0100 IL0007200111 1.7151% BORALEX INC -A NPV CA09950M3003 1.7039% OSAKI ELECTRIC CO LTD NPV JP3187600006 1.6793% HD HYUNDAI ELECTRIC & Energy System Co Ltd KRW5000 KR7267260008 1.6453% INFINEON TECHNOLOGIES AG NPV DE0006231004 1.6274% ACCIONA SA EUR1 ES0125220311 1.5958% ALFEN BEHEER B.V. EUR0.1 NL0012817175 1.5607% SINBON ELECTRONICS CO LTD TWD10 TW0003023008 1.5348% PRYSMIAN SPA EUR0.1 IT0004176001 1.5253% VESTAS WIND SYSTEM DKK 0.20 DK0061539921 1.5227% MERSEN EUR2 FR0000039620 1.511% LITTELFUSE INC USD0.01 US5370081045 1.4822% WESCO INTERNATIONAL INC USD0.01 US95082P1057 1.4608% GRENERGY RENOVABLES NPV ES0105079000 1.4429% VAISALA OYJ- A SHS NPV FI0009900682 1.4178% LG ENERGY SOLUTION KRW 500.0000 KR7373220003 1.4134% ORSTED A/S DKK10 DK0060094928 1.4063% ATKORE INC. USD 0.01 US0476491081 1.3963% ENERGIX-RENEWABLE ENERGIES NPV IL0011233553 1.3911% NKT A/S DKK20 DK0010287663 1.385% NEXANS SA EUR1 FR0000044448 1.3821% IMCD NV EUR0.16 NL0010801007 1.3747% SUMITOMO ELECTRIC INDUSTRIES NPV JP3407400005 1.3712% TKH GROUP NV-DUTCH CERT EUR0.25 NL0000852523 1.3632% DAIHEN CORP NPV JP3497800007 1.3588% VALMONT INDUSTRIES USD1 US9202531011 1.3545% CADELER A/S NOK 1.0000 DK0061412772 1.349% TOCALO CO LTD NPV JP3552290003 1.3441% ENERGIEKONTOR AG NPV DE0005313506 1.333% ELIA GROUP NPV BE0003822393 1.3317% WASION GROUP HOLDINGS LTD HKD0.01 KYG9463P1081 1.3131% ARCADIS NV EUR0.02 NL0006237562 1.3094% HYDRO ONE LTD NPV CA4488112083 1.3031% SCATEC ASA NOK0.025 NO0010715139 1.298% EDP RENOVAVEIS SA EUR5 ES0127797019 1.2876% CORP ACCIONA ENERGIAS RENOVA EUR NPV ES0105563003 1.2819% ERG SPA EUR0.1 IT0001157020 1.2809% DEME GROUPEUR NPV BE0974413453 1.2786% SSAB AB-A SHARES SEK8.8 SE0000171100 1.2762% TERNA SPA EUR0.22 IT0003242622 1.2561% HUBBELL INC USD0.01 US4435106079 1.2467% TIMKEN CO NPV US8873891043 1.2435% TOYO TANSO CO LTD NPV JP3616000000 1.2425% LANDIS+GYR GROUP AG CHF10 CH0371153492 1.2396% ALLIS ELECTRIC CO LTD TWD10 TW0001514008 1.2266% SPIE SA EUR0.47 FR0012757854 1.2222% MERIDIAN ENERGY LTD NPV NZMELE0002S7 1.2124% SCHNEIDER ELECTRIC SE EUR4 FR0000121972 1.2038% SHIHLIN ELECTRIC & ENGINEER TWD10 TW0001503001 1.1856% FORTUNE ELECTRIC CO LTD TWD10 TW0001519007 1.1756% REXEL SA EUR5 FR0010451203 1.1691% QUANTUMSCAPE CORP USD 0.0001 US74767V1098 1.1546% TORAY INDUSTRIES INC NPV JP3621000003 1.117% LEM HOLDING SA-REG CHF0.5 CH0022427626 1.1071% VOLTRONIC POWER TECHNOLOGY TWD10 TW0006409006 1.086% JL MAG RARE-EARTH CO LTD -H HKD 1.0000 CNE1000055Y4 1.0855% TECO ELECTRIC & MACHINERY TWD10 TW0001504009 1.0711% TA YA ELECTRIC WIRE & CABLE TWD10 TW0001609006 1.0581% SKF AB-B SHARES SEK2.5 SE0000108227 1.0569% CHINA DATANG CORP RENEWABL-H HKD 1.0000 CNE100000X69 0.9743% BELDEN INC USD0.01 US0774541066 0.9259% FLUENCE ENERGY INC USD 0.0100 US34379V1035 0.8817% WILLDAN GROUP INC USD 0.0100 US96924N1000 0.8062% EOS ENERGY ENTERPRISES INC USD 0.0001 US29415C1018 0.7373% Cash and/or Derivatives -0.0287%

The The Invesco GBP Corporate Bond UCITS ETF (distribution) aims to provide the total return performance of the Bloomberg Sterling Liquid Corporate Bond Index.

The L&G Global Quality Dividends UCITS ETF is a London listed ETF whose investment objective of the Fund is to provide exposure to companies with higher than average dividend and quality characteristics in developed market countries

Fund size (24 Apr 2026) $152.1m

Courtesy of Legal and General Investment Management

Courtesy of Legal and General Investment Management

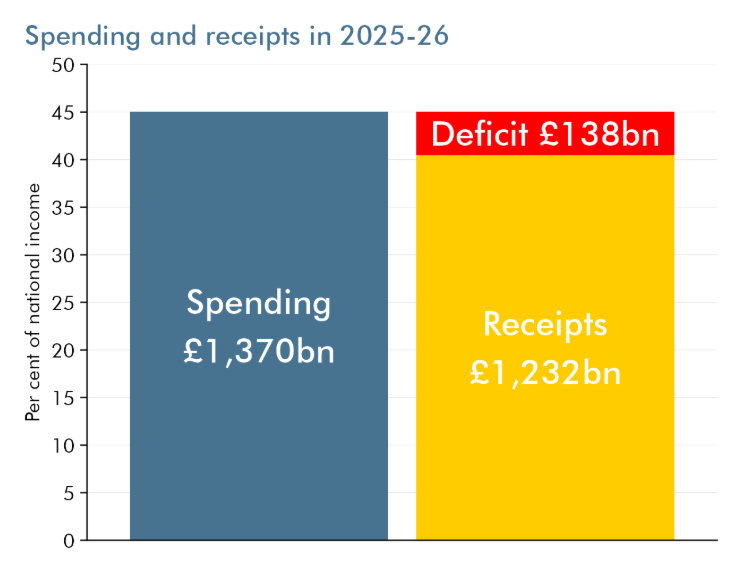

[1]. £138bn of borrowing to bridge the gap from Tax Revenue into HM Treasury and HM Government spending is £11.5bn a month. Yes, the Government has to borrow £11.5bn a month as tax revenues are not enough.

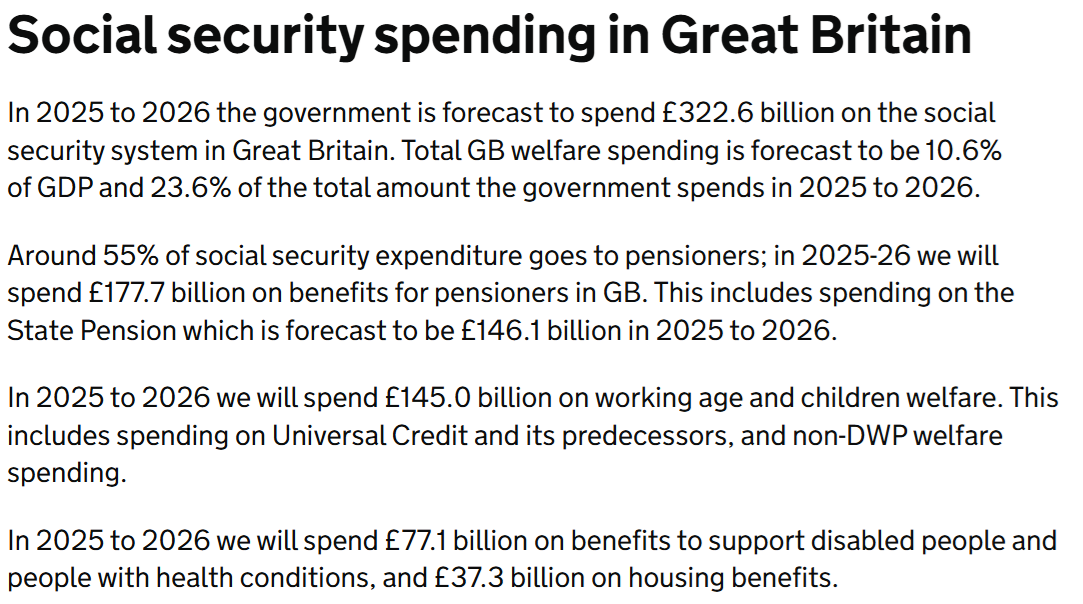

[2]. Government spending on Welfare = £322bn and total Government spending of £1370bn means:

(£322bn/1370bn) = 23.5% of all Government spending is on Welfare payments.

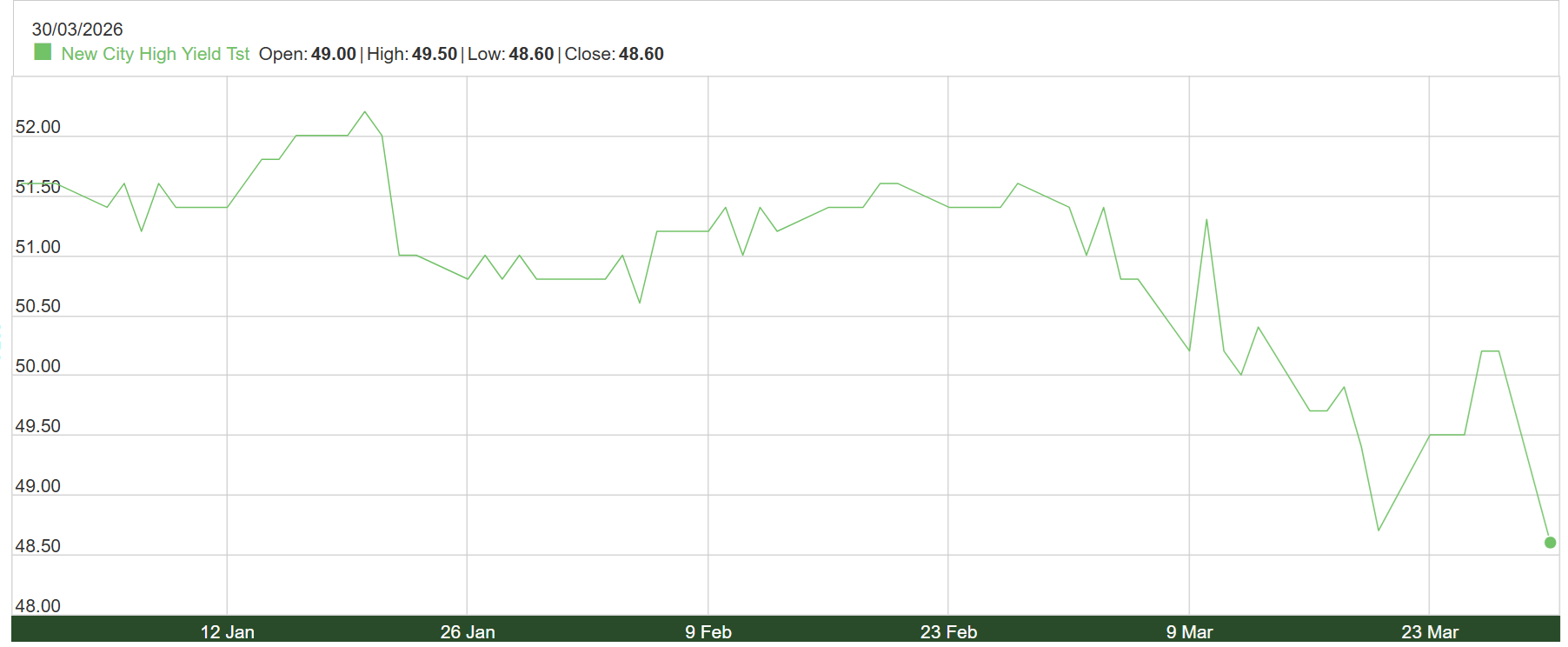

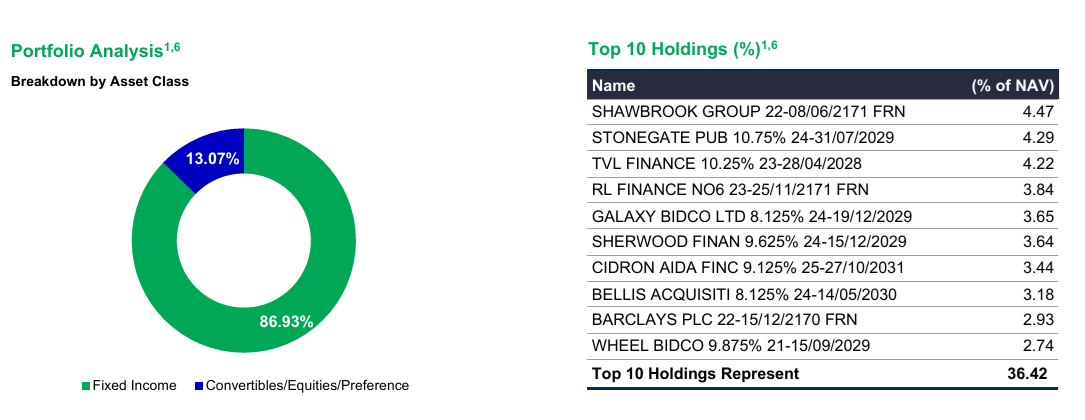

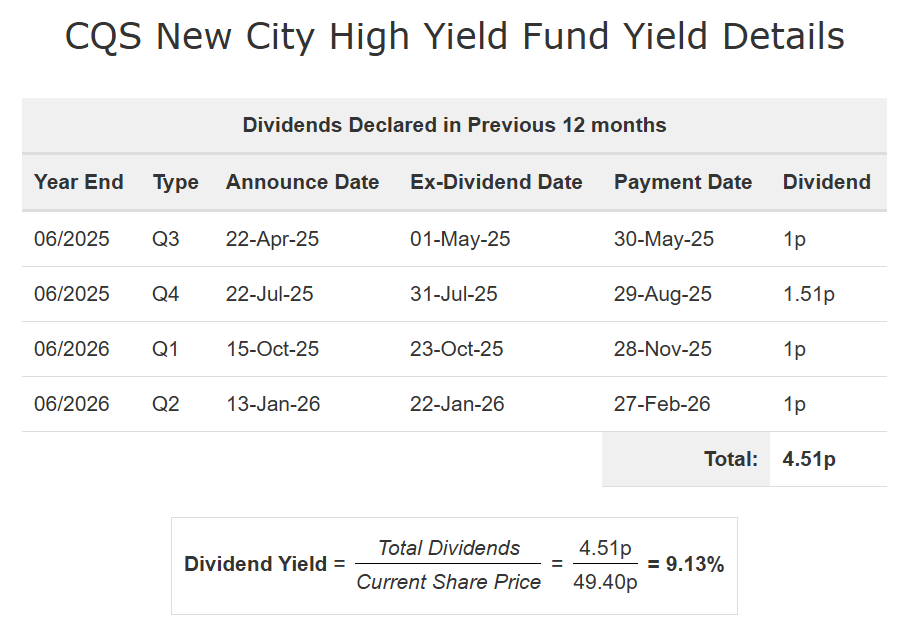

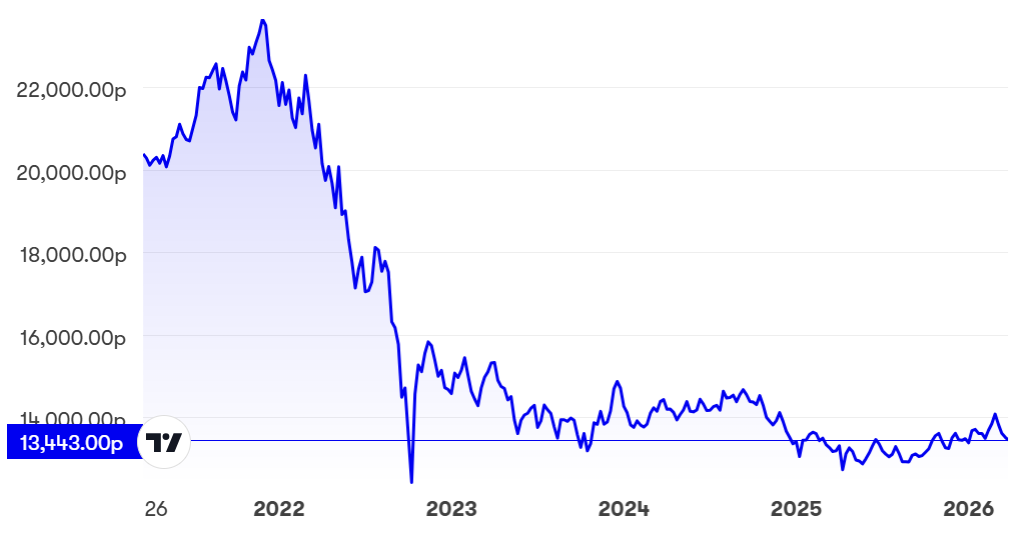

The CQS New City High Yield Fund Limited is a Jersey domiciled closed ended investment company whose objective is to provide investors with a high dividend yield and the potential for capital growth by investing mainly in high-yielding fixed interest securities.

The Amundi UK Government Inflation-Linked Bond UCITS ETF is a UCITS compliant exchange traded fund that aims to track the benchmark index FTSE Actuaries Govt Securities UK Index Linked TR All Stocks.

Assets Under Management (AUM) : £79.72 ( million GBP )

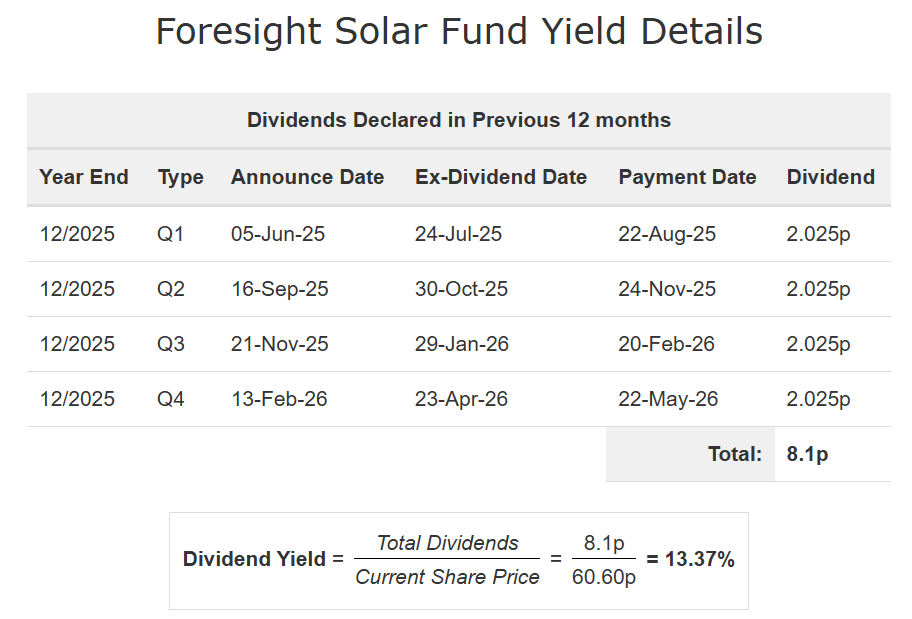

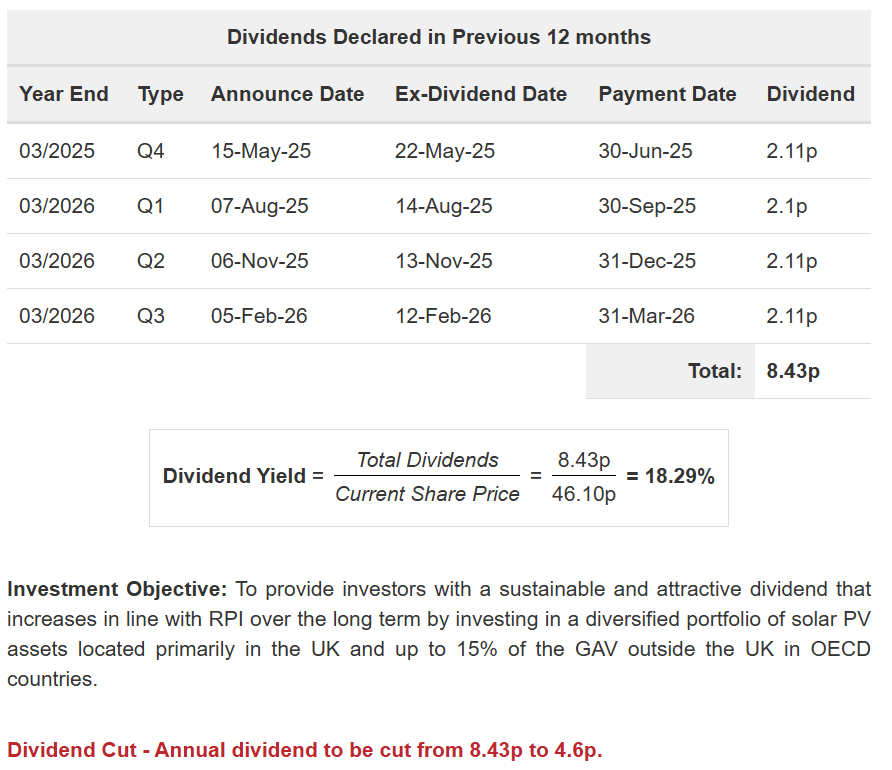

Foresight Solar’s aims to provide investors with a sustainable, progressive quarterly dividend and enhanced capital value, whilst facilitating climate change mitigation and the transition to a lower carbon economy.

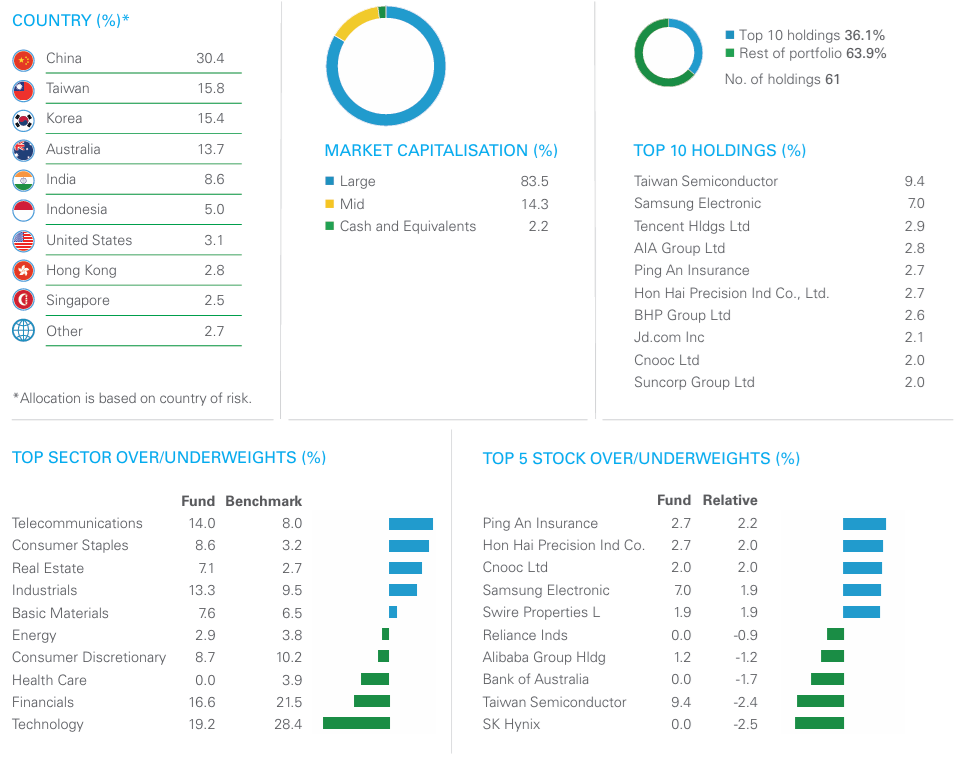

The M&G India Fund is an investment fund, The fund aims to provide combined income and capital growth that is higher than that of the Indian stockmarket (as measured by the MSCI India Index), net of the ongoing charge figure, over any five-year period. At least 80% of the fund is invested in the shares and equity-related instruments of companies that are incorporated, listed, domiciled or do most of their business in India

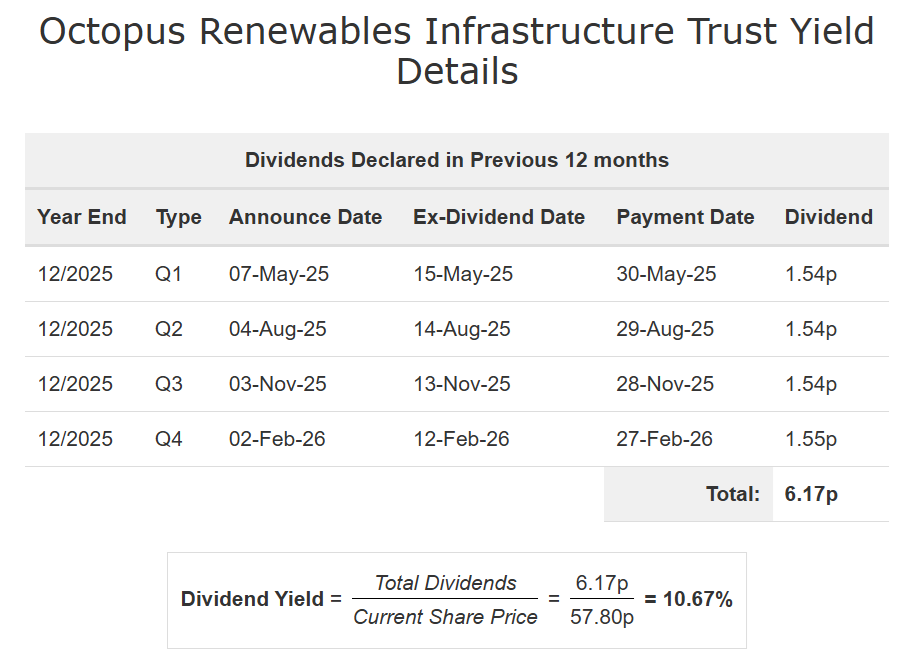

The Octopus Renewables Infrastructure Trust plc is a London listed investment trust. It is an investment company focused on providing investors with an attractive and sustainable level of income returns, with an element of capital growth, by investing in a diversified portfolio of Renewable Energy Assets across Europe, the UK and Australia

“Third, there’s a real risk artificial intelligence could widen wealth inequality if ownership does not broaden alongside it. When we talk about the economic disruption of AI, most of the conversation is about jobs. That’s an enormously important question, and one that goes beyond economics. Work provides income, purpose, and dignity. But history suggests that transformative technologies create enormous value—and much of that value accrues to the companies that build and deploy them, and to the investors who own them. The economy is rewarding scale like never before. In industry after industry, we’re seeing more divergent, “K-shaped” outcomes, where leading firms pull further ahead while others struggle to keep pace. The contrast can be striking: Walmart reached its highest-ever valuation, two weeks after Saks went bankrupt. AI may accelerate this trend further. The companies with the data, infrastructure, and capital to deploy AI at scale are positioned to benefit disproportionately. That is not unusual, and none of this is inherently problematic. Market leadership has always shifted with technological change. The broader question is who participates in the gains. When market capitalization rises but ownership remains narrow, prosperity can feel increasingly distant to those on the outside.”

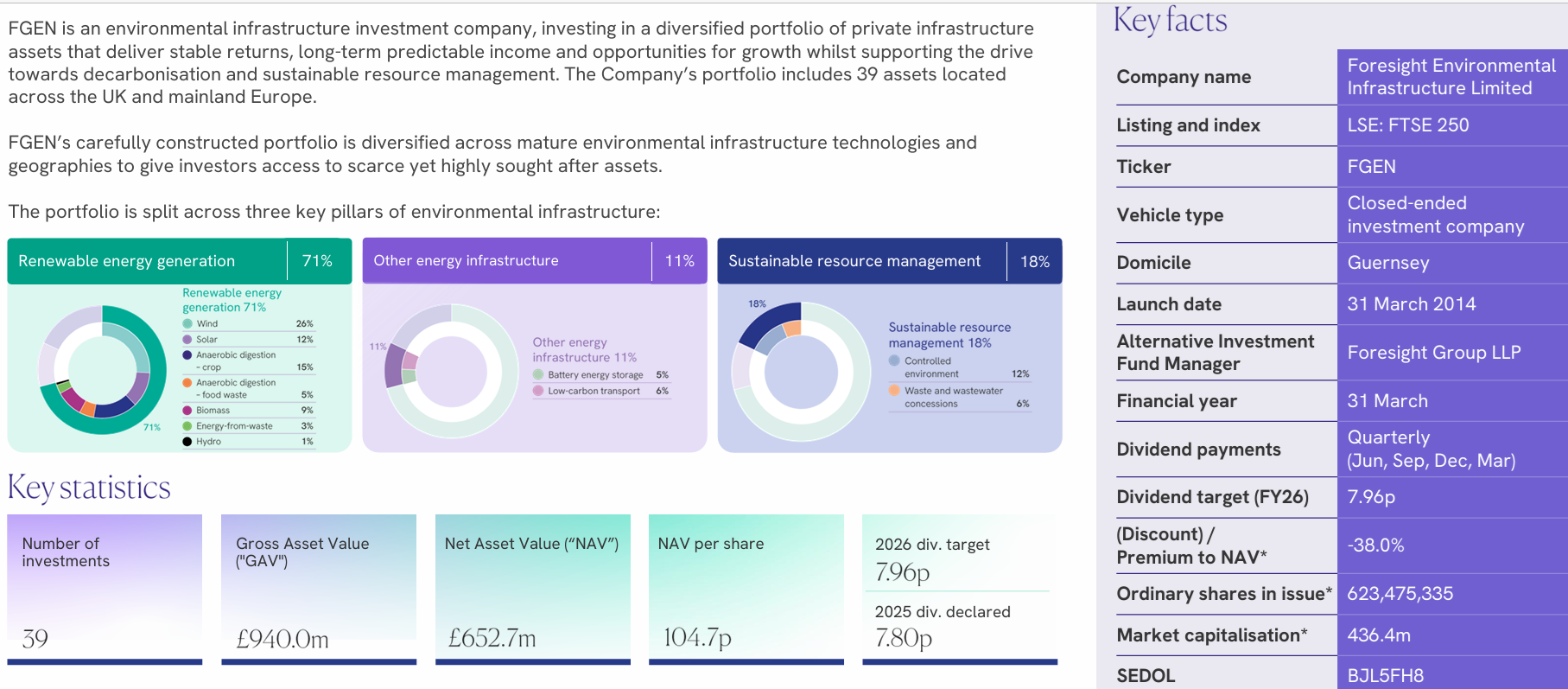

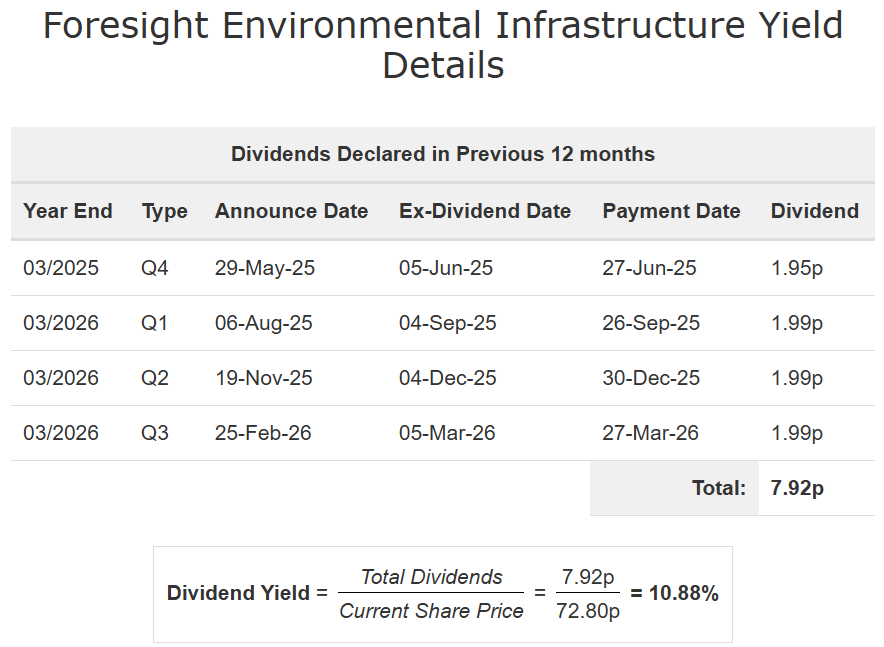

The Foresight Environmental Infrastructure Limited is a London listed investment trust.

Foresight Environmental Infrastructure, formerly JLEN Environmental Assets Group and John Laing Environmental Fund, is a large British investment trust dedicated to investments in Renewable Energy Infrastructure.

Courtesy of Foresight Environmental Infrastructure PLC

The NextEnergy Solar Fund is a London listed investment trust. NextEnergy Solar Fund (“NESF”) is a renewable energy investment company listed on the main market of the London Stock Exchange and is a constituent of the FTSE 250. NextEnergy Solar Fund invests primarily in utility scale solar assets, alongside complementary ancillary technologies, like energy storage.

The Global X SuperDividend ETF accesses up to 100 of the highest dividend paying equities around the world. The ETF seeks to make distributions on a monthly basis

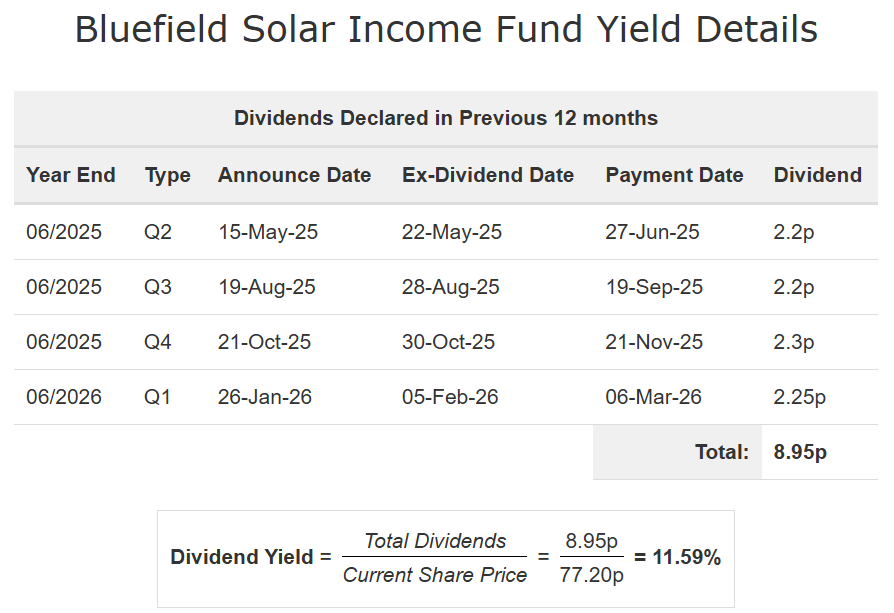

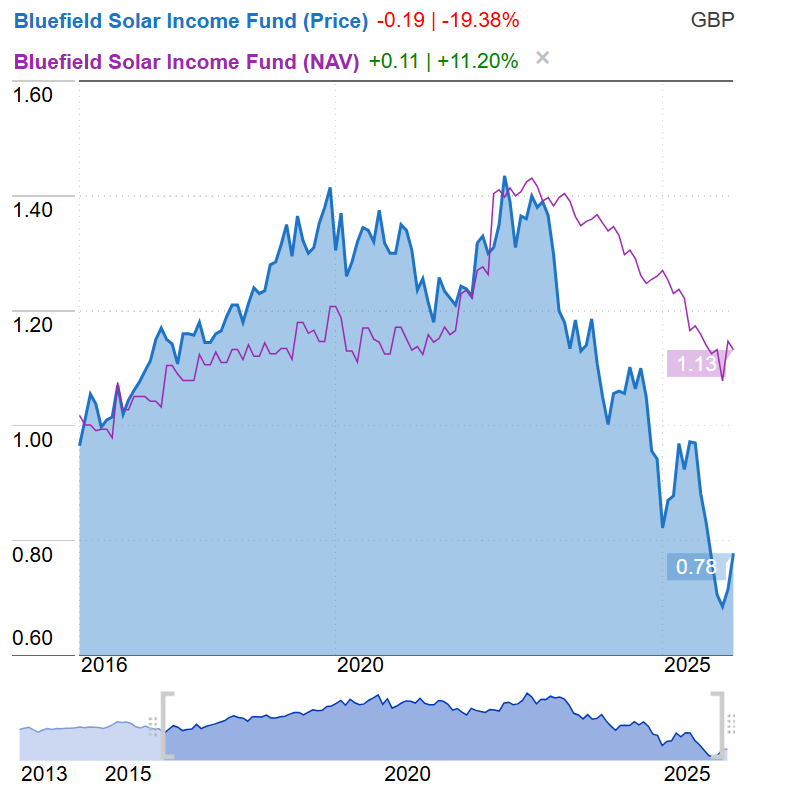

The Bluefield Solar Income Fund is a London listed investment trust that invests in UK solar farms. Bluefield Solar Income Fund (BSIF) is a pioneer in the renewable energy space. It primarily targets utility-scale solar, wind and energy storage assets and portfolios on greenfield, industrial and/or commercial sites. BSIF aims to deliver long-term stable dividends and has one of the most successful track records in the sector.

BSIF seeks to provide shareholders with an attractive return. This is mainly in the form of quarterly income distributions through being invested primarily in renewable energy assets in the UK.

The BlackRock American Income Trust Plc in a London listed investment trust whose objective is to provide long-term capital growth, whilst paying an attractive level of income.

The L&G Market Neutral Commodities UCITS ETF has the investment objective to provide a long/short exposure to a broad base of futures contracts on physical commodities.

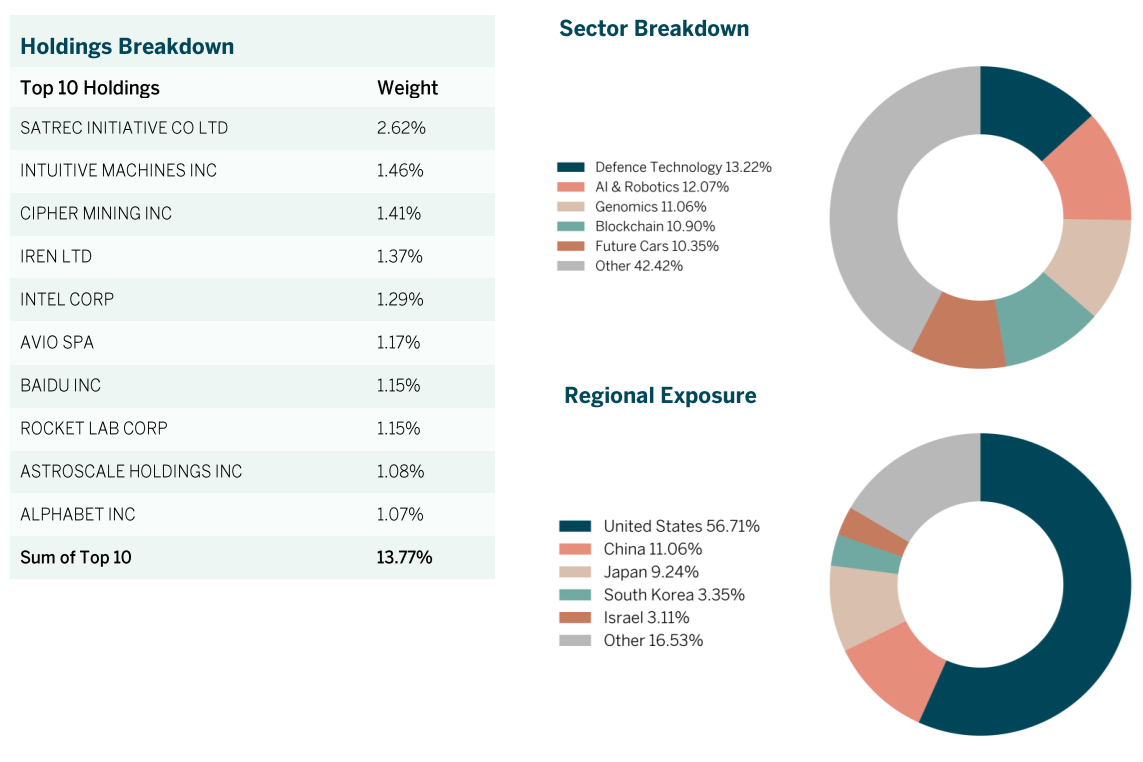

The HAN -GINS Tech Megatrend Equal Weight UCITS ETF invests to provide exposure to the disruptive technology companies in “Industry 4.0” that are changing the world through global megatrends. The tech megatrend ETF provides equal weight access to companies that are driving innovation in eight sub -sectors including Robotics & Automation, Cloud Computing & Big Data, Cyber Security, Future Cars, Genomics, Social Media, Blockchain, Digital Entertainment, Defence Technology and Quantum Computing.

The iShares MSCI Korea UCITS ETF USD (Acc) is a fund that gives exposure to a broad range of companies in Korea, that gives the investor a single country exposure and offers a direct investment in Korean companies.

Today, Thursday 5th Feb 2026, Vodafone, the UK’s 2nd telecommunications company (BT being the premier player https://www.bt.com), pays out its dividend.

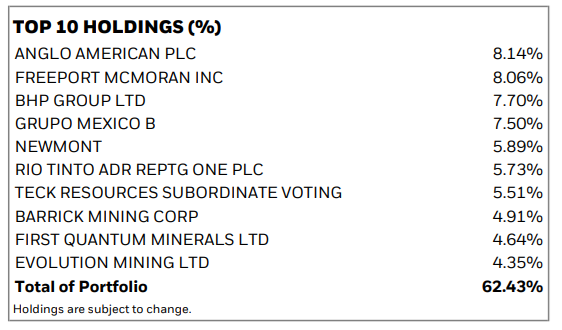

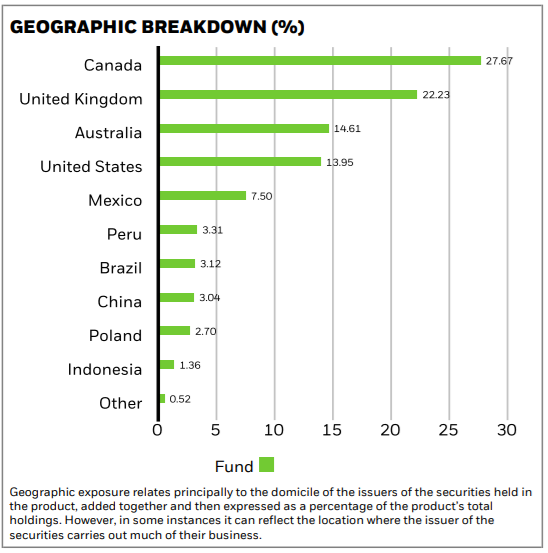

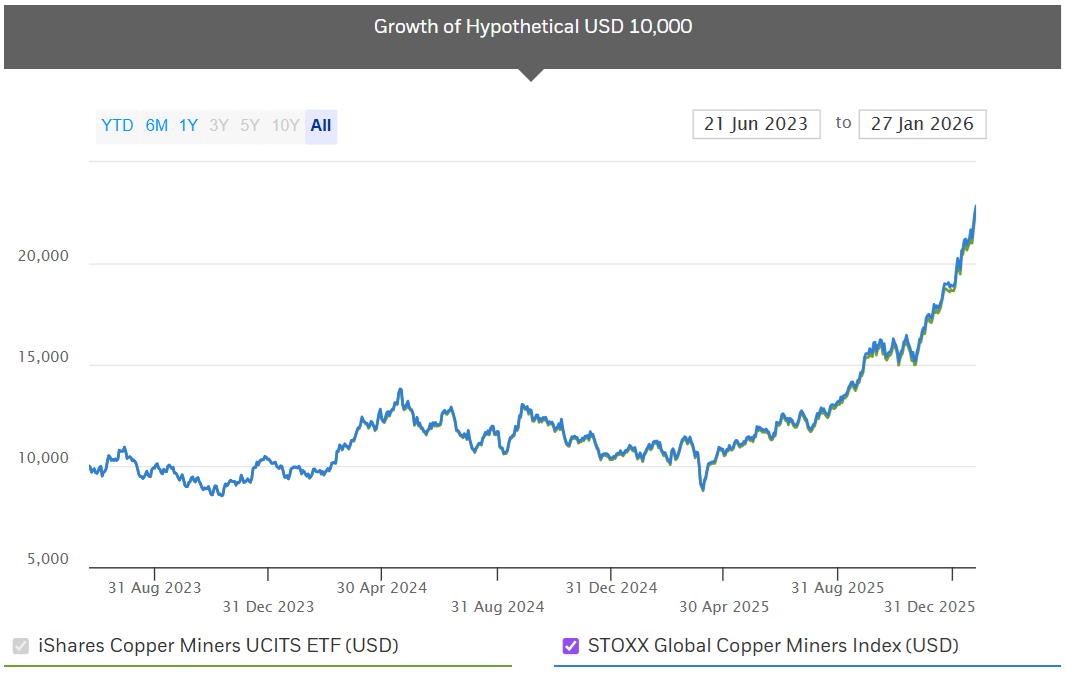

The fund (iSHARES COPPER MINERS UCITS ETF) aims to achieve a return on your investment, through a combination of capital growth and income on the Fund’s assets, which reflects the return of the STOXX Global Copper Miners Index, the Fund’s benchmark index (Index).

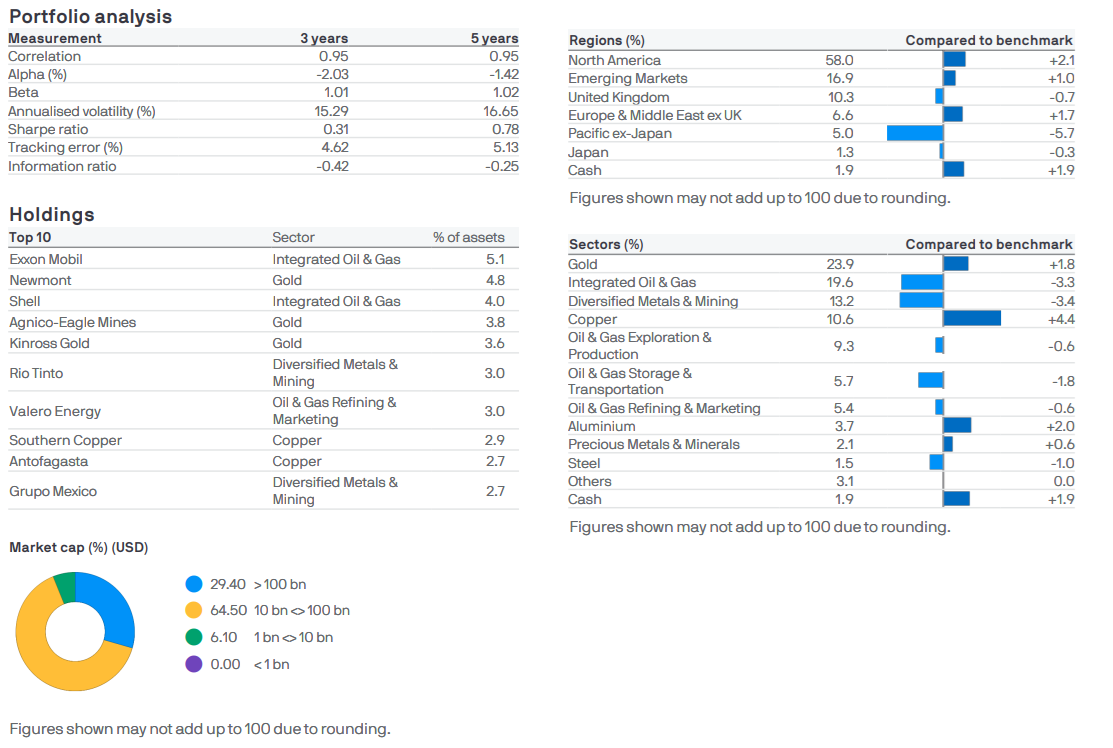

The JPM Natural Resources Fund aims to provide capital growth over the long-term (5-10 years) by investing at least 80% of the Fund’s assets in the shares of companies throughout the world engaged in the production and marketing of commodities.

US Government Sold $654 Billion of Treasuries, week commencing Monday 12th January 2025.

In the week, the US Government sold $654 billion in Treasury securities spread over 9 auctions, including 10-year Treasury notes and 30-year Treasury bonds.

Of these auction sales, $500 billion were Treasury bills with maturities from 4 weeks to 26 weeks, most of them to replace maturing T-bills.

Type

Auction date

Billion $

Auction yield

Bills 6-week

Jan-13

77.5

3.585%

Bills 13-week

Jan-12

88.8

3.570%

Bills 17-week

Jan-14

69.2

3.560%

Bills 26-week

Jan-12

79.5

3.580%

Bills 4-week

Jan-15

95.3

3.595%

Bills 8-week

Jan-15

90.3

3.600%

Bills

$500.5Billion

And of these $654 billion in auction sales, $154 billion were notes and bonds, including $50 billion in 10-year Treasury notes.

Notes & Bonds

Auction date

Billion $

Auction yield

Notes 3-year

Jan-12

74.9

3.609%

Notes 10-year

Jan-12

50.4

4.173%

Bonds 30-year

Jan-13

28.4

4.825%

Notes & bonds

$153.6Billion

Added up, this is $654 Billion, in US Government borrowings. The US Government has to borrow, as the taxes collected are not enough to fund the US Federal Government’s spending commitments, and thus borrows.

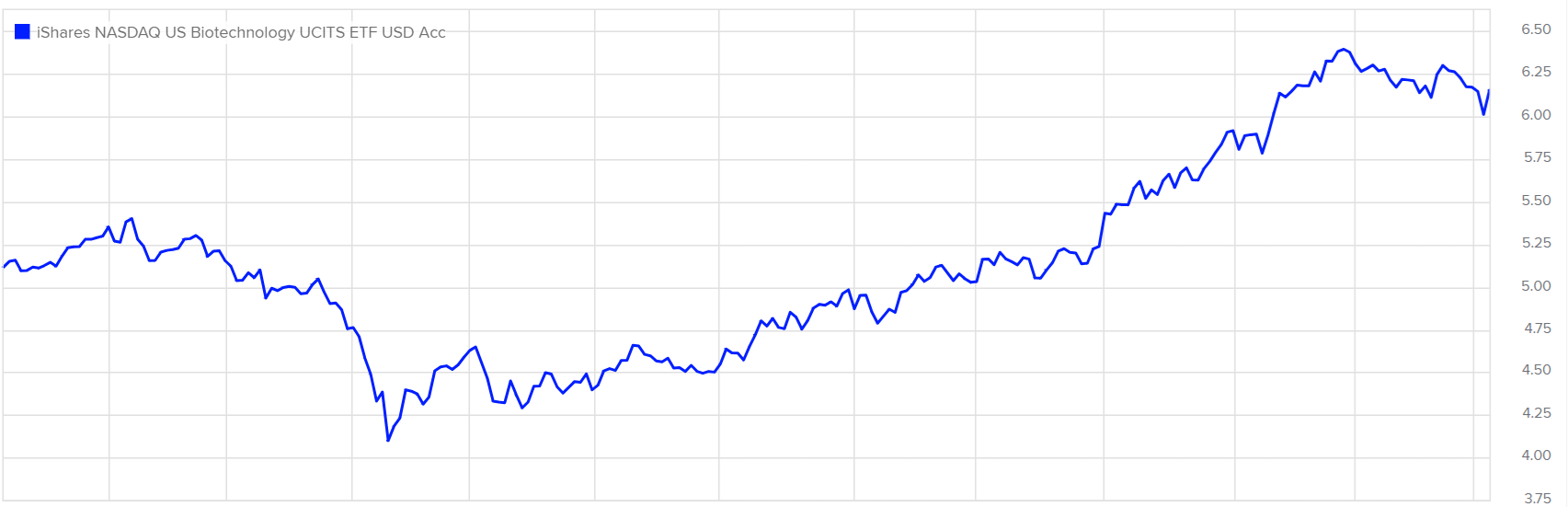

The iShares Nasdaq US Biotechnology UCITS ETF seeks to track the investment results of an index composed of biotechnology and pharmaceutical equities listed on the NASDAQ.

FromToTotal ReturnThis is an input box to enter up to four benchmarks that you want to compare with the base ric.Use left and right arrow keys to navigate, enter to create, delete to delete tags Only list items can be added as tagsThis is an input box to enter up to ten indicators.Use left and right arrow keys to navigate, enter to create, delete to delete tags Use up and down arrow keys to navigate list items and enter to add a new tag Only list items can be added as tags

Cordiant Digital Infrastructure is the first UK-listed investment company to provide investors with dedicated exposure to the core infrastructure of the digital economy.

Verizon job cuts are equal to 20% of non-union employee wage costs

Wireless company to convert 179 company-owned retail stores to franchise operations

Verizon to create $20 million fund to assist laid off employees with job search, skills in AI era

WASHINGTON, Nov 20 (Reuters) – U.S. wireless carrier Verizon (VZ.N) on Thursday said it will cut more than 13,000 jobs in its largest single layoff as it works to shrink costs and restructure operations.

Tomorrow the Chancellor of the Exchequer will announced the long awaited budget. For weeks we have seen the bond market reacting to ill timed and ill advised leaks, undermining confidence in the UK Gilt market. Lenders to UK Government have to have confidence in the UK able to pay on the debts outstanding, and also lenders need to have confidence in the UK to lend new money.

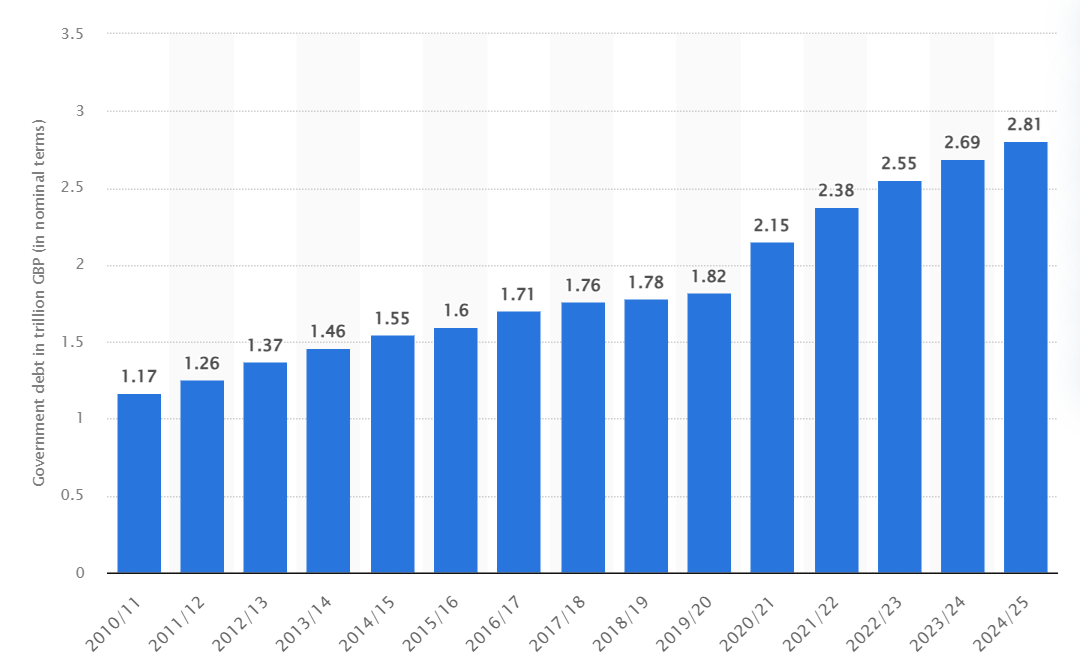

When the government spends more than it receives in tax and other revenues it borrows to cover the difference. This borrowing is known as ‘public sector net borrowing’ but is often referred to as the deficit.

Total public sector net debt in the United Kingdom from 2010/11 to 2024/25

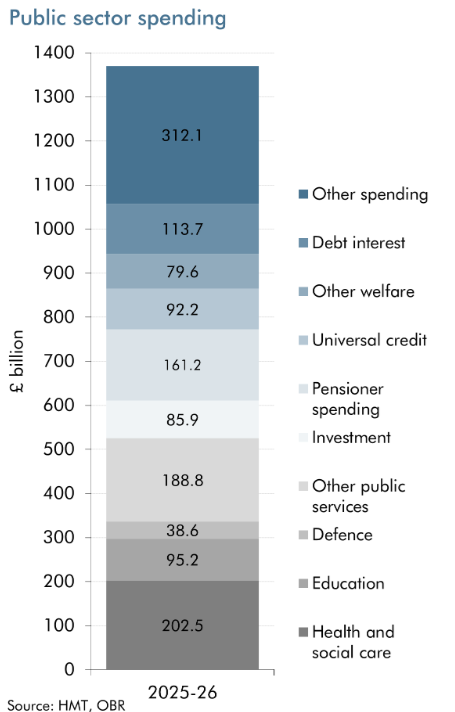

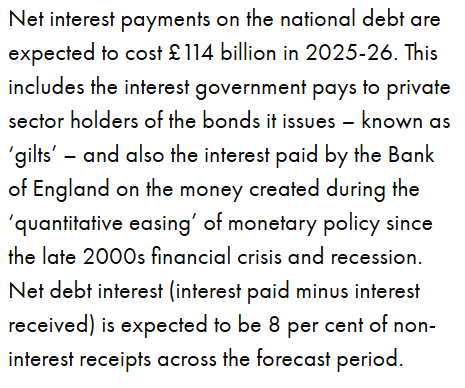

One can see each year the HM Government has been spending more than it earns in taxation over the last 15 years. This is NOT sustainable. Consequently, debt interest payments are now above £100 billion a year, and the OBR has warned that, without action, debt could rise to 270 per cent of GDP by the early 2070s. Note, £100 billion interests is money that can NOT be paid finance our brave armed forces, or build new schools.

In 2024-25, it is expected public spending to amount to £1,278.6 billion, and thus out of that £1278 billion, £100 billion is on debt interest.

Also we are seeing huge media speculation on whether the Chancellor of the Exchequer will break the election promise in the party manifesto of not increase taxes, and this speculation has now become normalised on social media with arm chair political economists saying the Chancellor of the Exchequer will break an election pledge, these ‘experts’ have zero knowledge of the importance of the bond market or a decent grasp of economics.

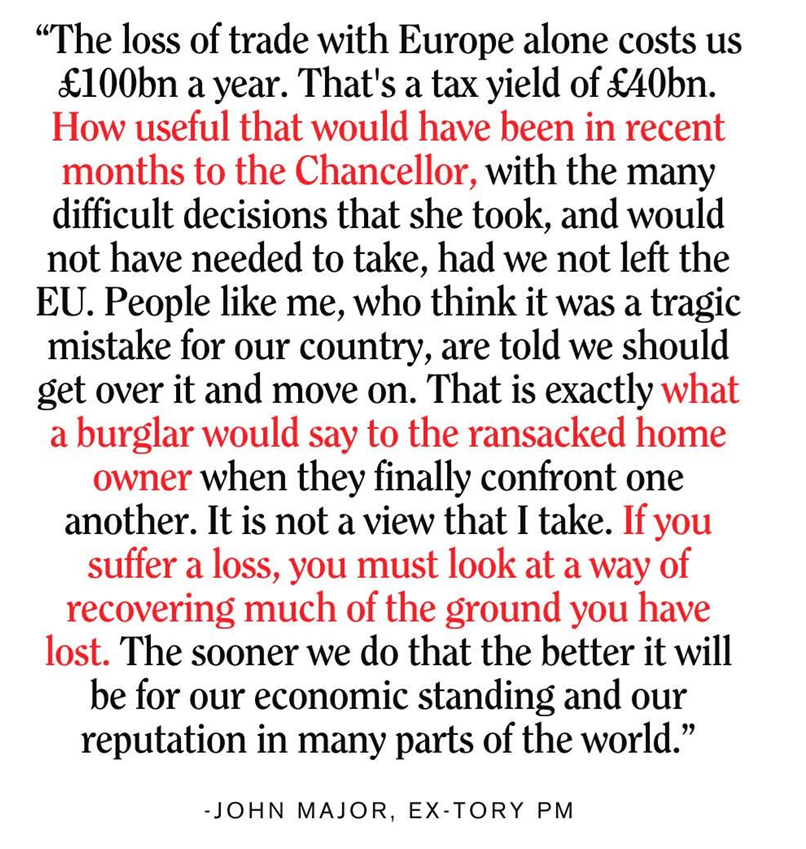

However in the interests of fairness and equality it was David Cameron who maintained his promiseand manifesto pledge to ask the UK population for the referendum on the UK continued membership the European Union, and he kept his promise:-

Courtesy of John Major

As shown above, keeping manifesto pledges is NOT a holy or sacred act.

The UK needs to raise taxes to be able to fund the annual budget deficit, if not, the UK Government can not actually fund day to day operations. It needs that funding to finance public services, and if we do NOT, we face a Liz Truss / Kwasi Kwarteng moment, where the UK struggles to raise money, with borrowing costs surge, as lenders get worried over economic competence and stewardship of the UK economy. Sadly, taxes will have to rise, and breaking that manifesto pledge is the right things to do for the UK Government to be able borrow from on the Bond Market and fund public services.

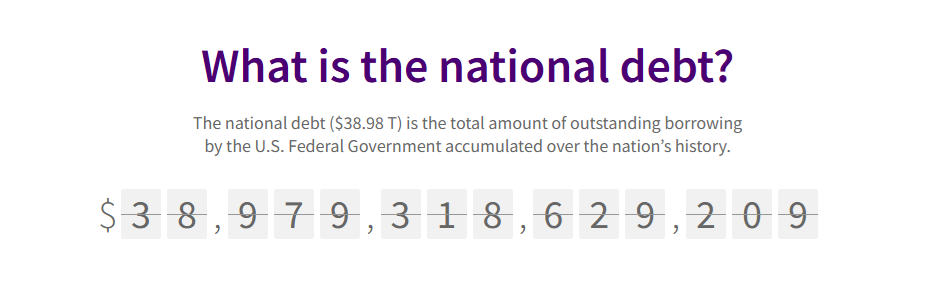

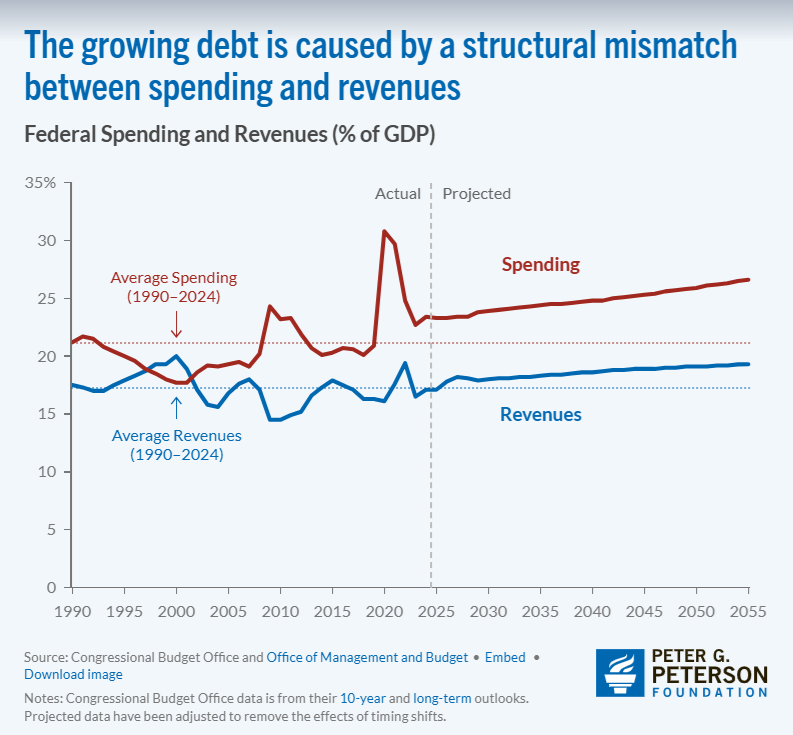

Why is the National Debt so high? America’s growing debt is the result of simple math — each year, there is a mismatch between spending and revenues. When the federal government spends more than it takes in, it has to borrow money to cover that annual deficit. And each year’s deficit adds to the USA’s growing national debt.

Historically, the largest deficits were caused by increased spending around national emergencies like major wars or the Great Depression. Today, deficits are caused mainly by predictable structural factors: our aging baby-boom generation, rising healthcare costs, higher interest rates, and a tax system that does not bring in enough money to pay for what the government has promised its citizens. Moving forward, it will be critical for America’s leaders to address our rising debt, and its structural factors, which are described below.

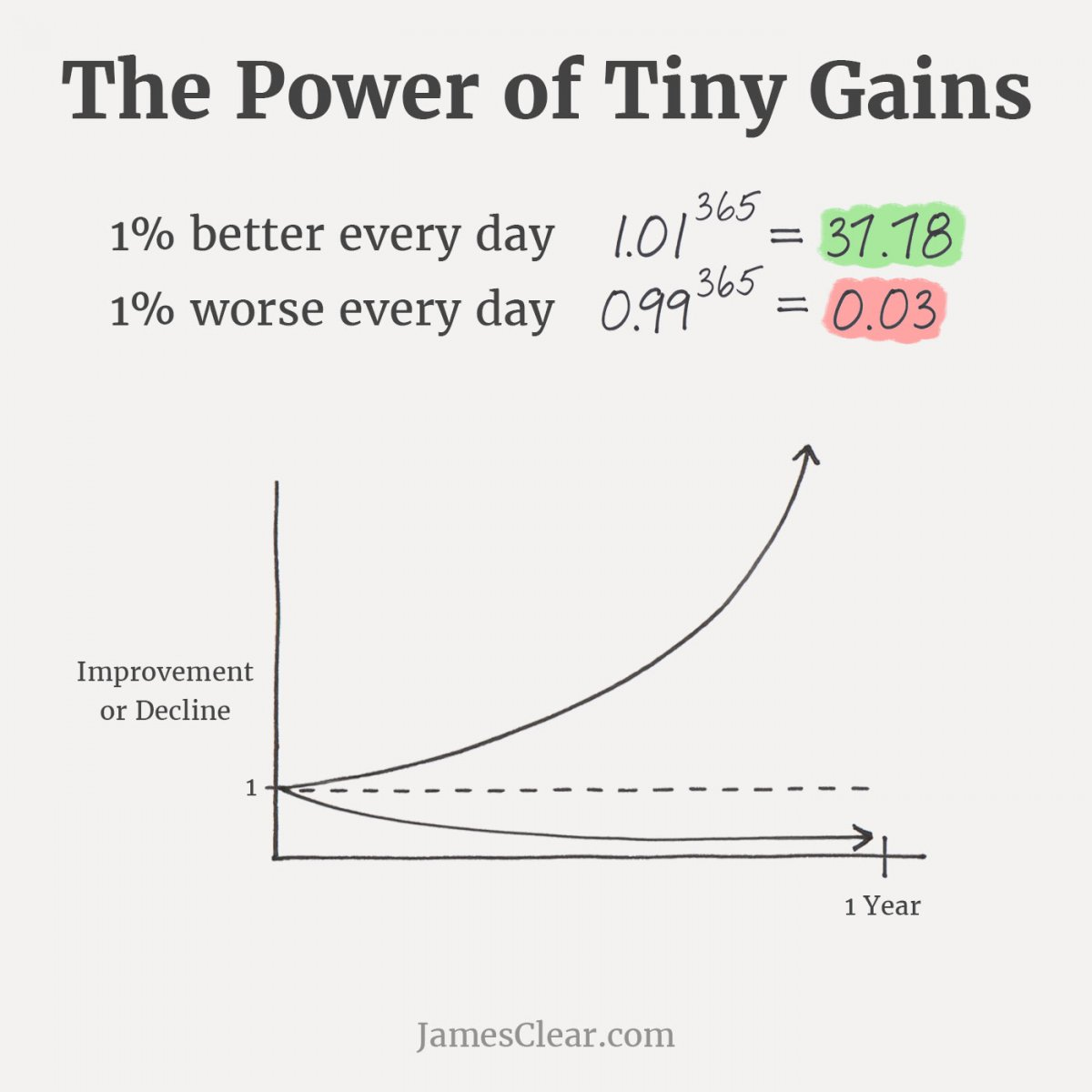

In the beginning, there is basically no difference between making a choice that is 1 percent better or 1 percent worse. (In other words, it won’t impact you very much today.) But as time goes on, these small improvements or declines compound and you suddenly find a very big gap between people who make slightly better decisions on a daily basis and those who don’t.

Here’s the punchline:

If you get one percent better each day for one year, you’ll end up thirty-seven times better by the time you’re done.

The L&G Multi-Strategy Enhanced Commodities ex-Agriculture & Livestock UCITS ETF is a London Listed ETF that aims to track the performance of the Barclays Backwardation Tilt Multi-Strategy Ex-Agriculture & Livestock Capped Total Return Index.

Fund size $88.4m

The fund provides broad-based exposure to commodities via a diversified basket of commodity futures with different expiry dates of up to 1 year.

The upside point of this fund:-

-Diversification Commodities are a distinct asset class with returns that are largely uncorrelated with stock and bond returns -Inflation hedge Commodity indices tend to benefit from rising inflation -Broad commodities exposure Basket of commodity futures, excluding Agriculture and Livestock, with dynamically determined expiry dates

Courtesy of Legal and General Investment Management

“The public sector employs 5.9 million people in the UK, at an annual cost of £270 billion in 2023–24 (including salaries, employer pension contributions and employer National Insurance contributions) – 10% of national income and 22% of total UK government spending. The employment, pay and productivity of these employees are therefore an important determinant of the material standard of living of millions of families, as well as a crucial input into the provision of public services. Public sector pay growth is an important pressure on public spending.”

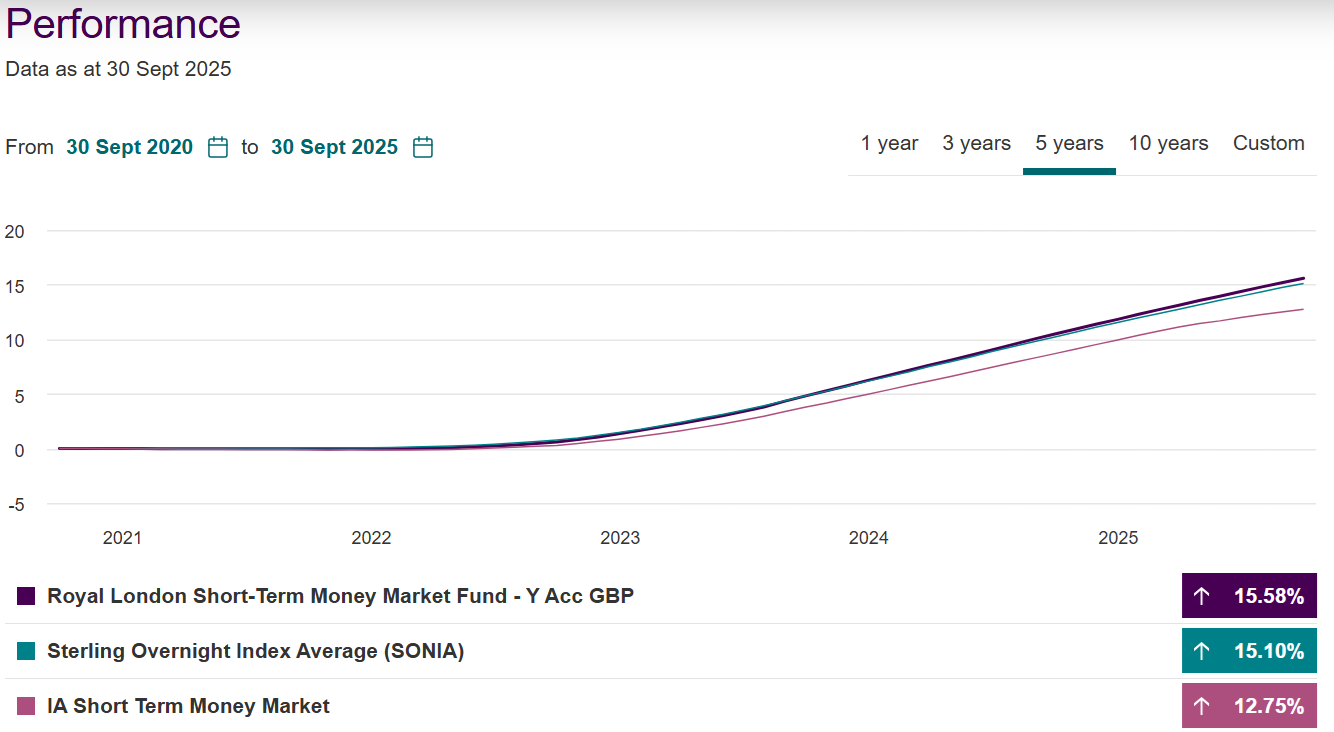

The Vanguard Sterling Short-Term Money Market Fund (the “Fund”) seeks to provide stability in the value of investments, liquidity and exposure to a variety of investments that typically perform differently from one another while maximising income earned from distributions such as interest

The Fund’s investment objective is to preserve capital and provide an income over rolling 12-month periods by predominantly investing (at least 80% of its assets) in cash and cash equivalents. The Fund’s comparator benchmark is the Bank of England Sterling Overnight Interbank Average (SONIA).